David's (BT) data blog

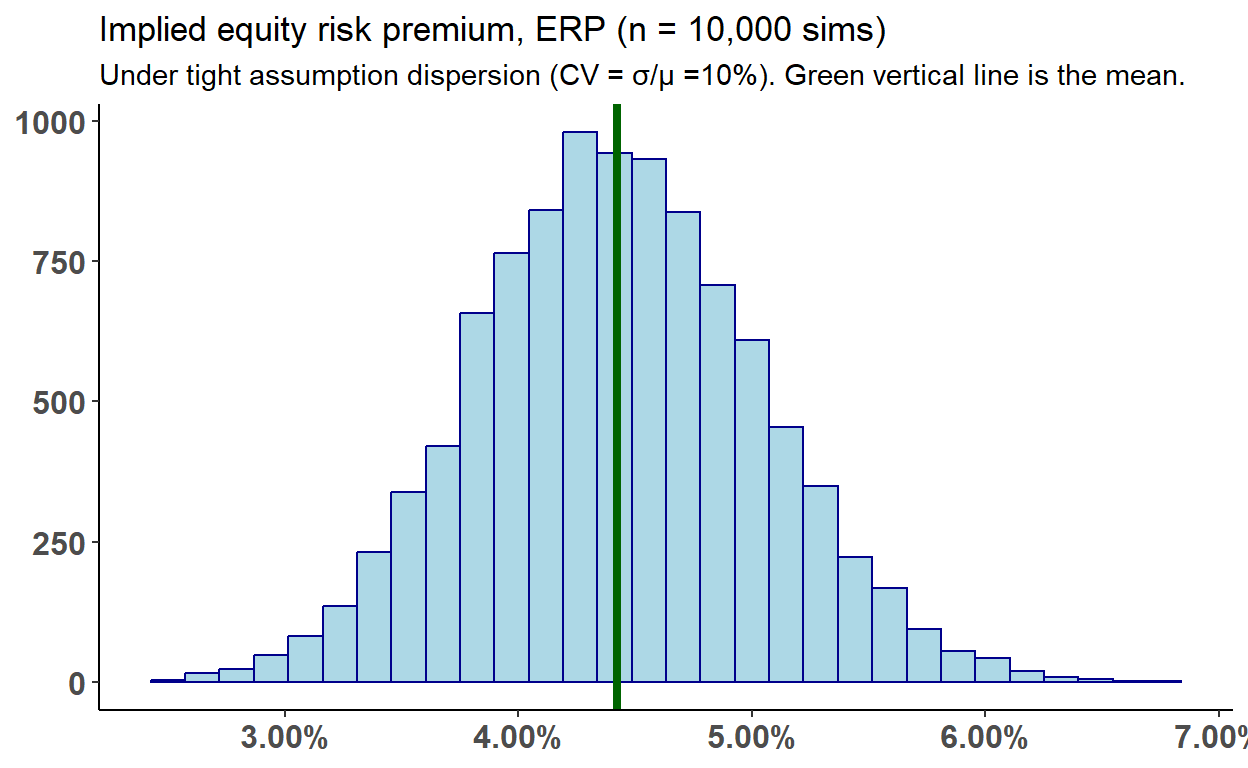

Simulating the equity risk premium

The implied ERP is very sensitive to assumptions, in particular G2

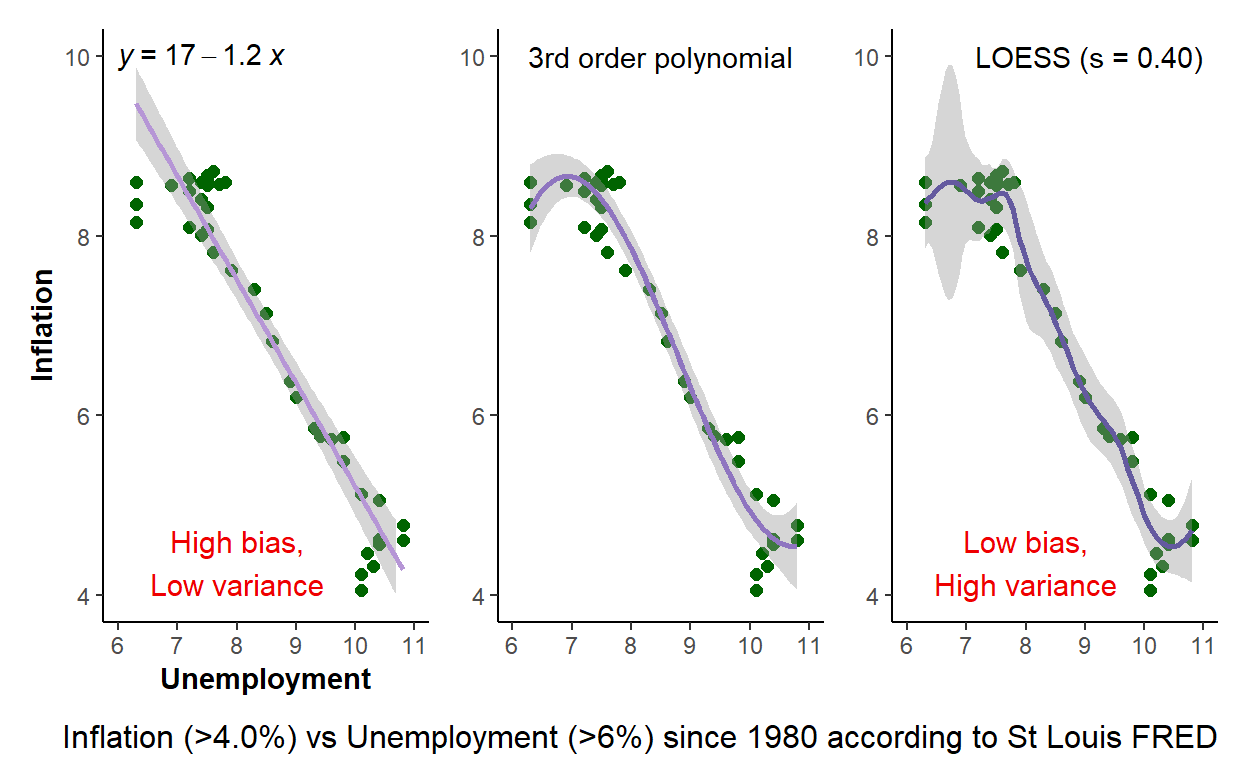

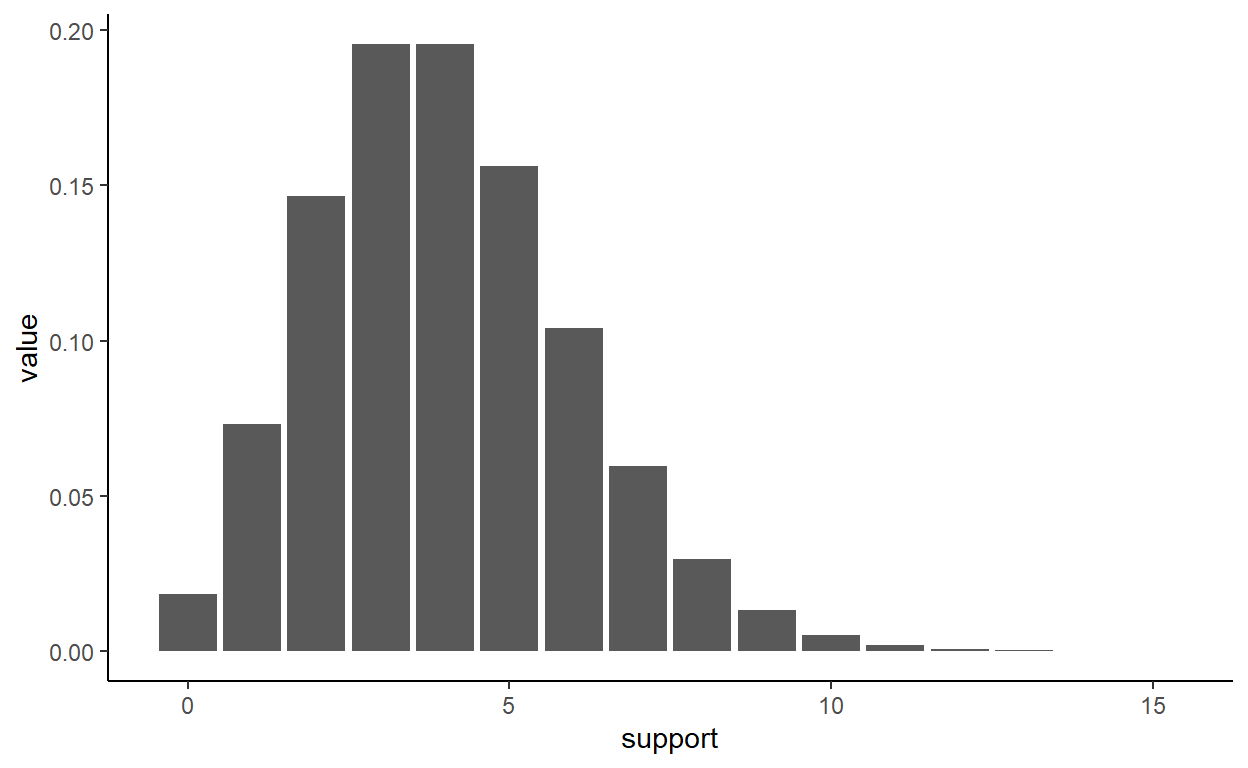

Phillips curve to illustrate bias-variance tradeoff

Underfitting implies low-variance but high-bias; overfitting implies low-bias but high variance

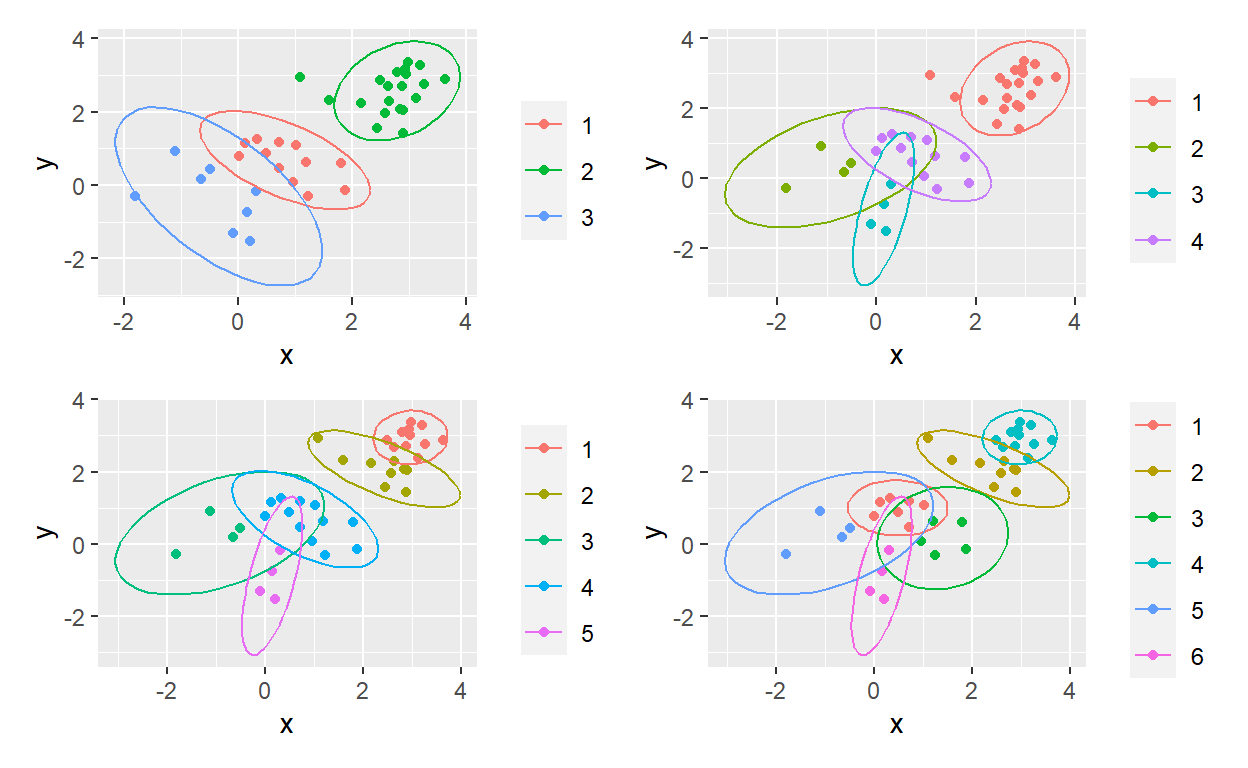

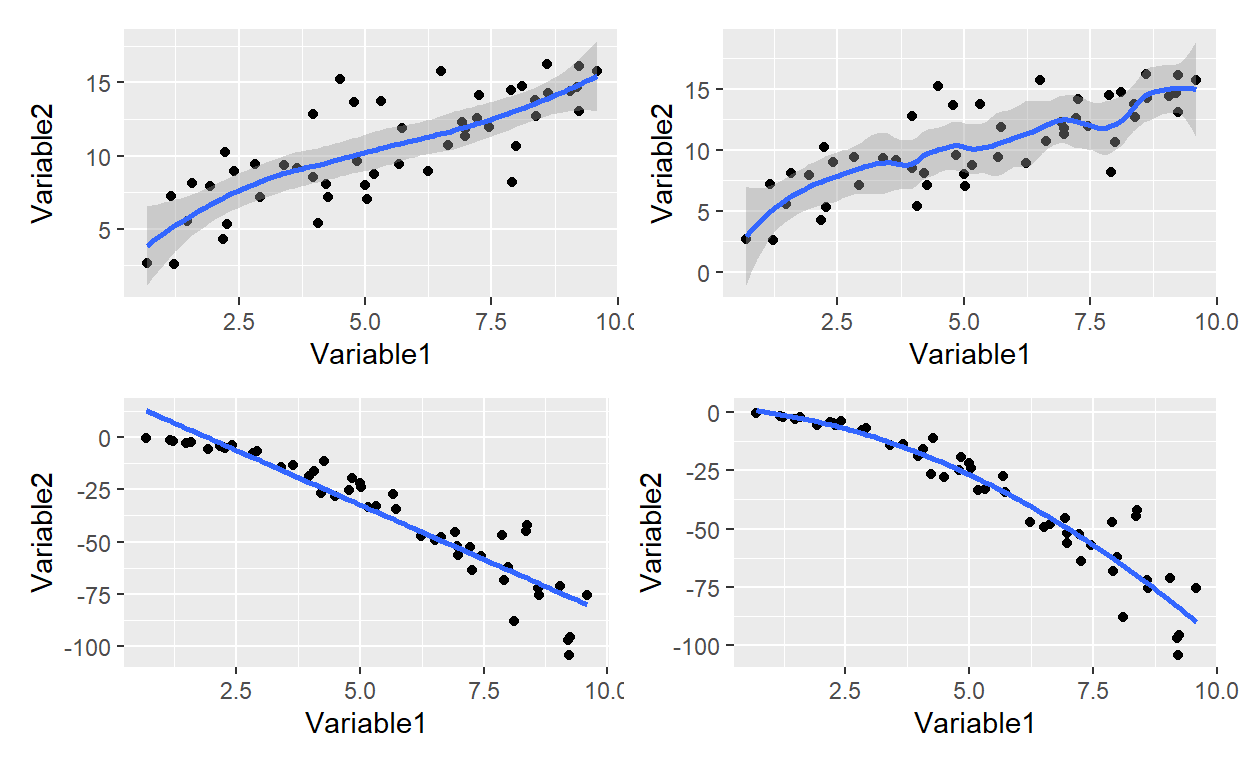

Using purrr to map over a range of k-means clusters

Mapping a k-means factory

Intermediate Functional Programming with purrr

My progress in learning how to purrr

Advanced Data Visualization with R at JH

The sequel in the JH dataviz specialization

Foundations of purrr

Map over list elements with elegance and power

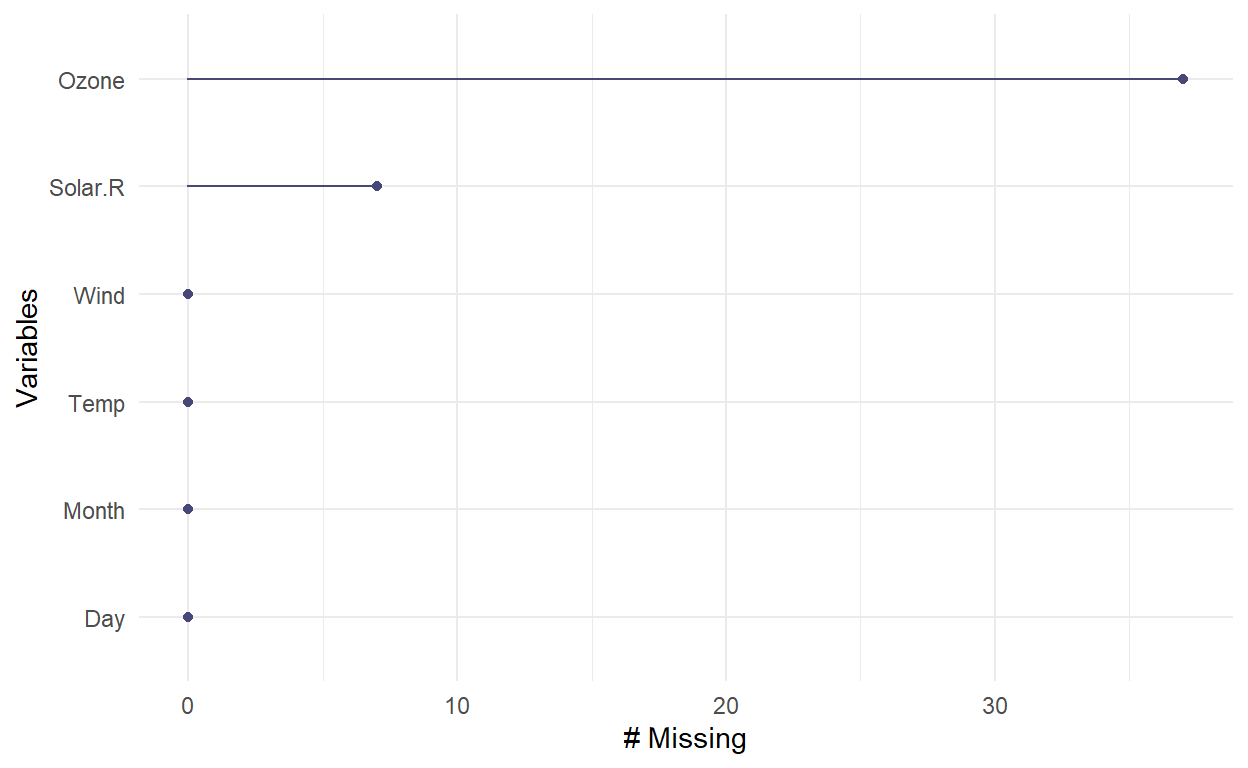

How to Process Missing Data

How do we visualize what's missing? And the art of imputation

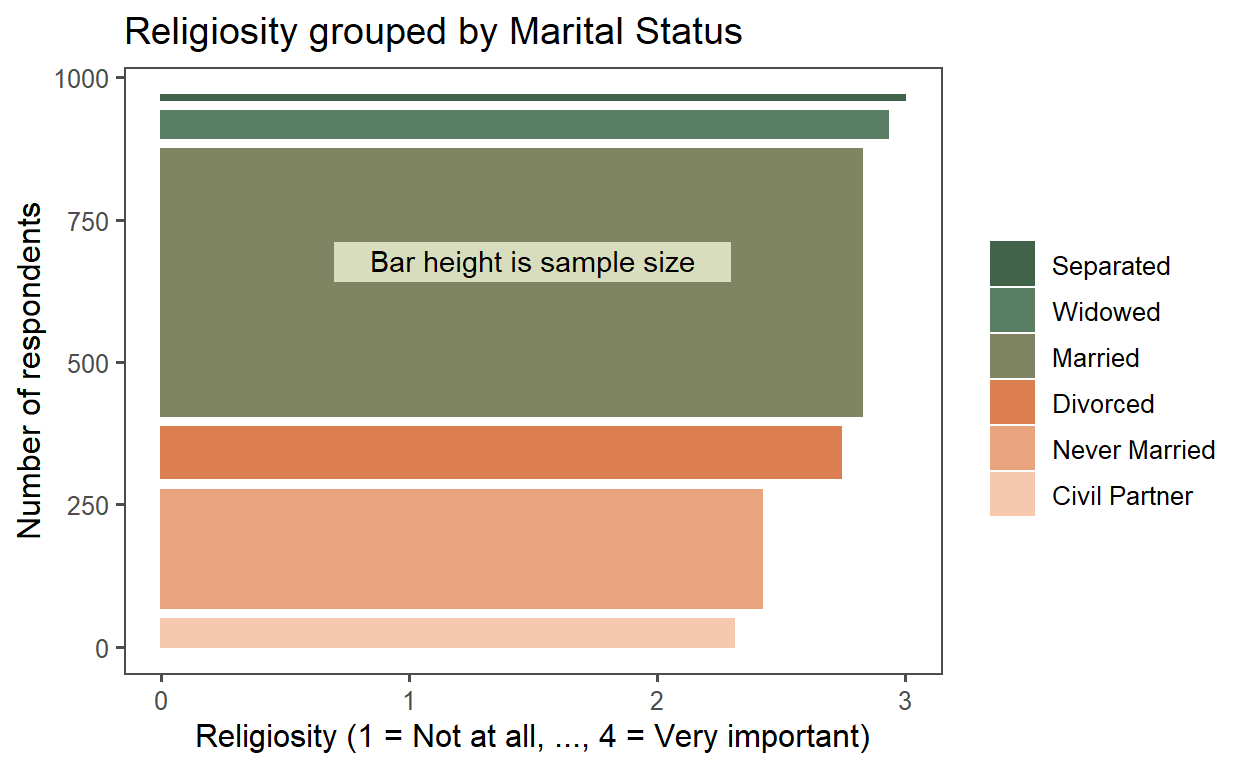

My JH dataviz submission

Product of JH's DataViz in R with ggplot2.

Example of embedded Excel snippet

Excel workbook (or ranges) can be embedded in the classic iframe

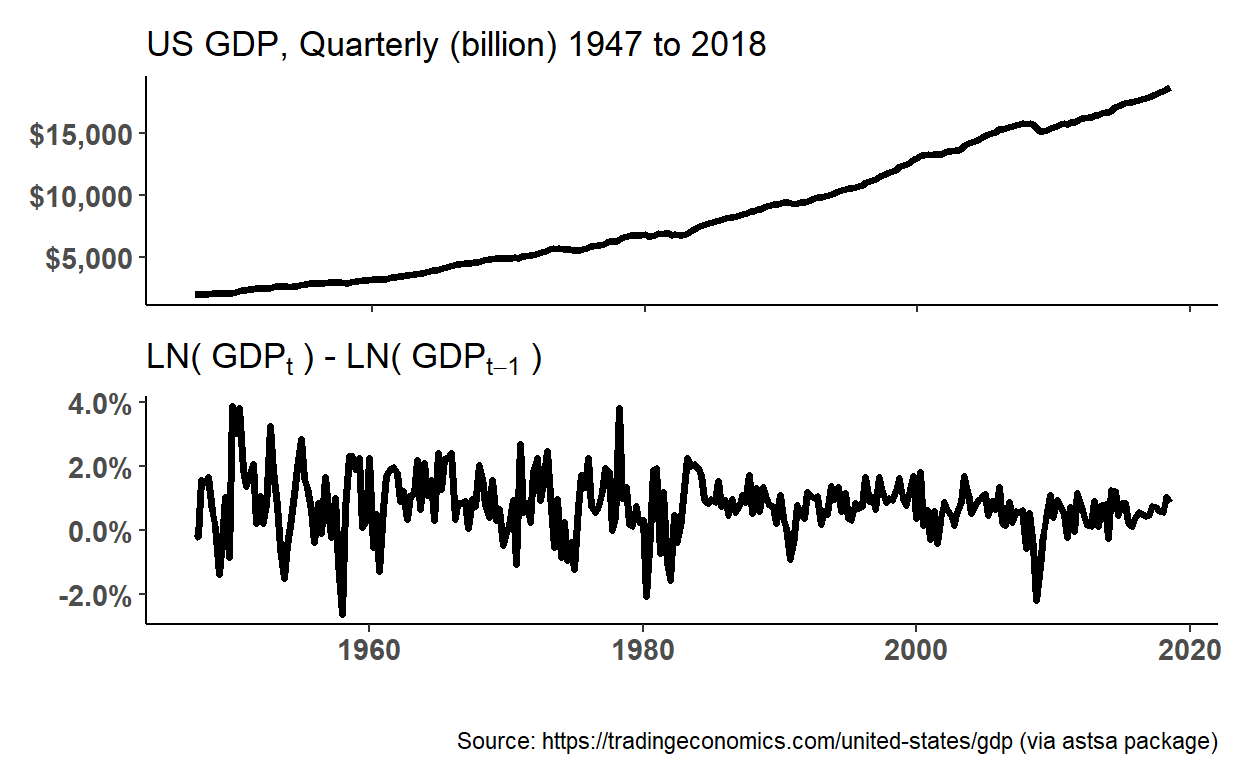

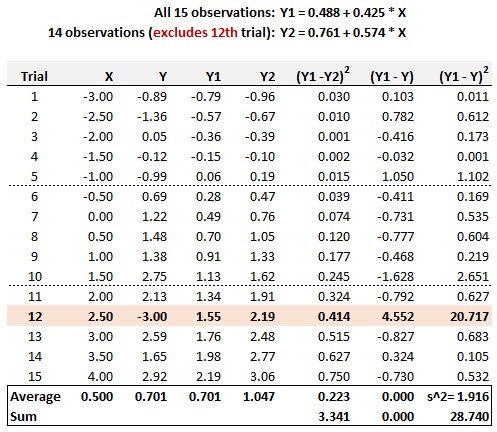

BT PQ P1.T2.21.1 (SET) Non-stationary time series (2021)

Seasonal dummy model, roots of characteristic equation, and transformation (difference versus detrend) of non-stationary process

BT PQ P1.T2.20.25 (SET) Long-horizon AR(p) MA(q) forecasts

The long-run mean of an MA(q) process is the intercept; of the AR(p) process is delta/(1 - sum of params)

BT PQ P1.T2.20.24.3 AIC and BIC

Penalized MSE measures are called information criteria (IC) and two popular such measures are the Akaike Information Crite-rion (AIC) and the Bayesian Information Criterion (BIC).

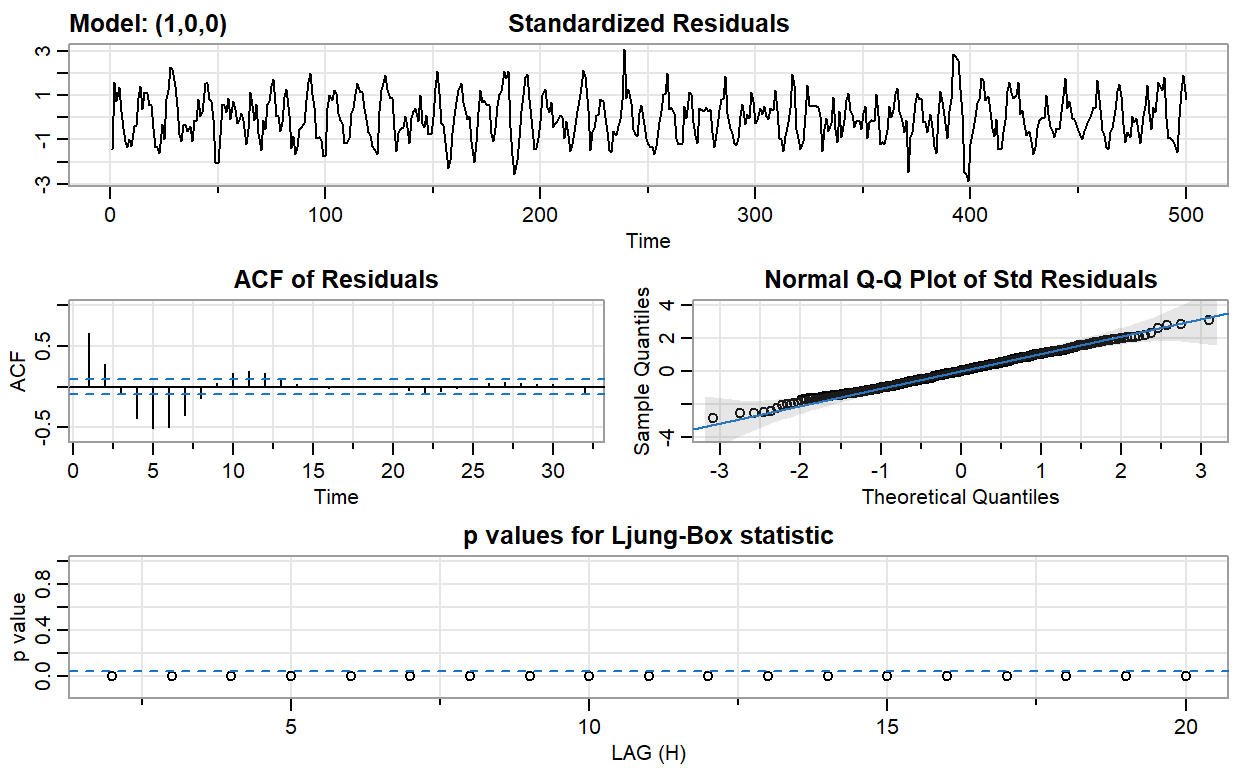

BT PQ P1.T2.20.24.2 Box-Pierce and the Ljung-Box tests

The Box-Pierce statistic is a simplified version of the Ljung-Box statistic; both are joint tests of autocorrelation

BT PQ P1.T2.20.23 (SET) autoregressive moving average (ARMA) models

ARMA(p,q) combines an AR(p) and MA(q)

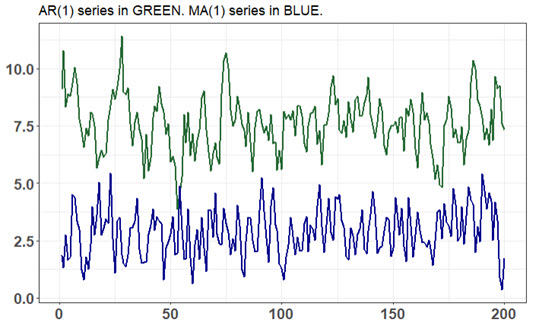

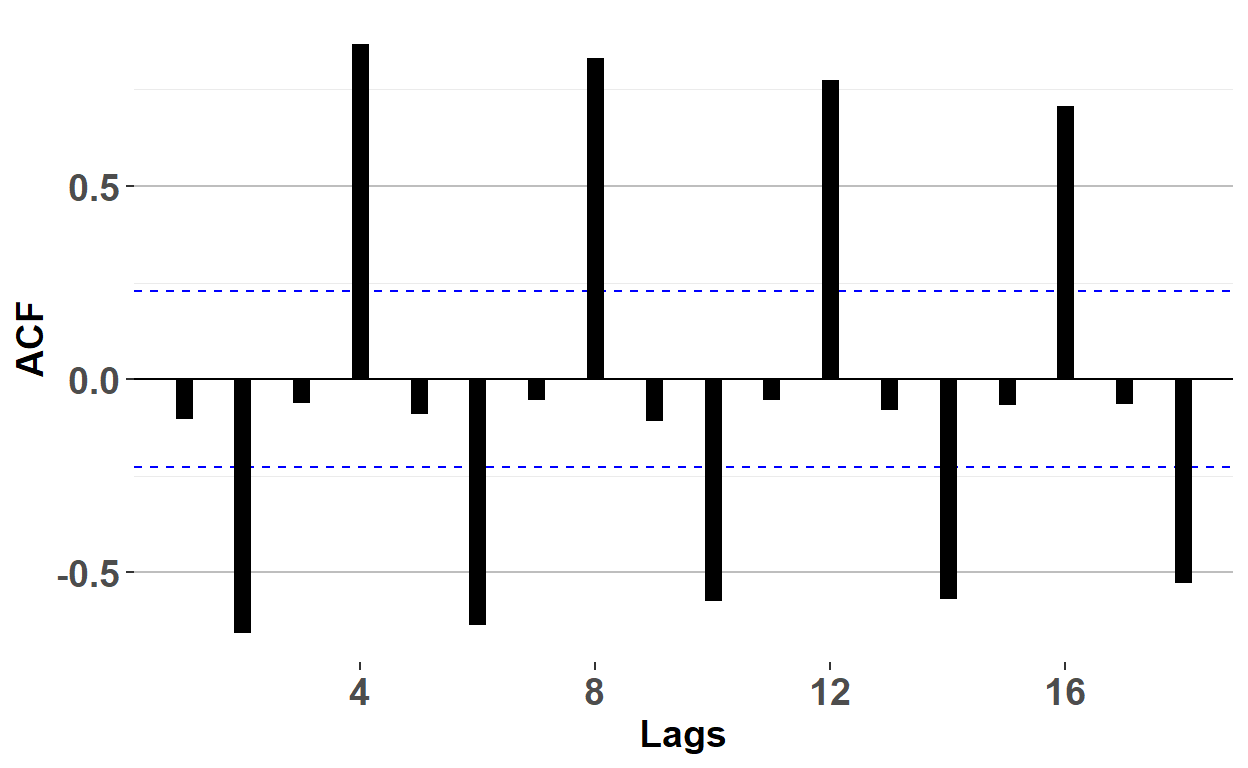

BT PQ P1.T2.20.22.2 autoregressive (AR) versus moving average (MA) process

What's the difference between and AR and MA process, when they appear to be similar?

BT PQ P1.T2.20.21.3 White Noise (WN) Process

White noise (WN) is the basic time series building block

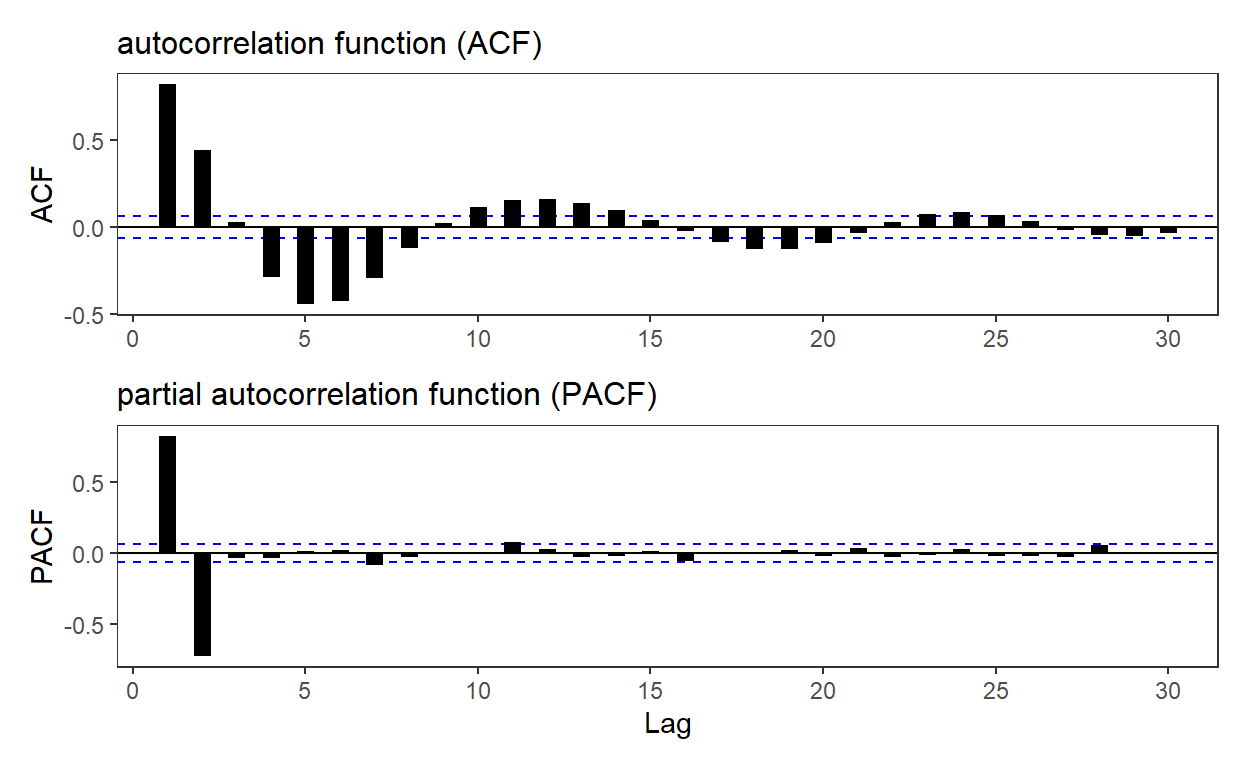

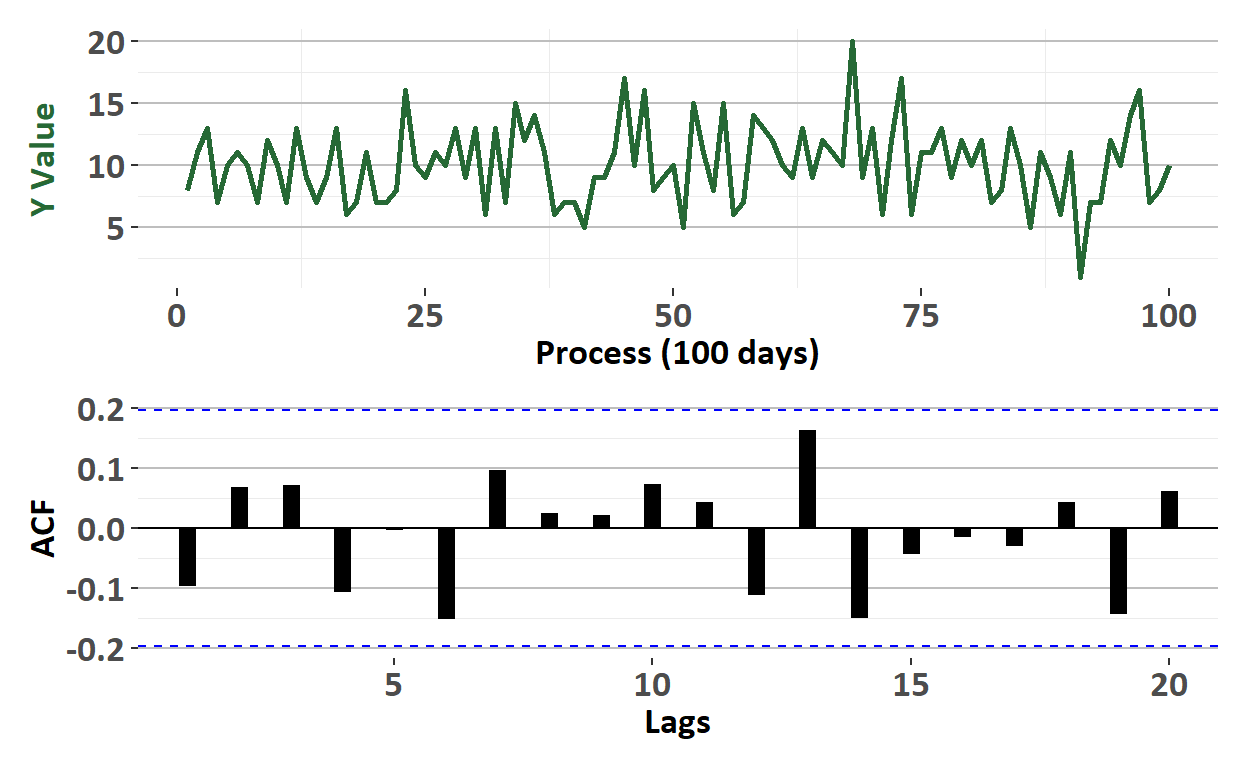

BT PQ P1.T2.20.21.2 Autocorrelation function (ACF)

The autocorrelation function (ACF; aka, correlogram) plots autocorrelation coefficients

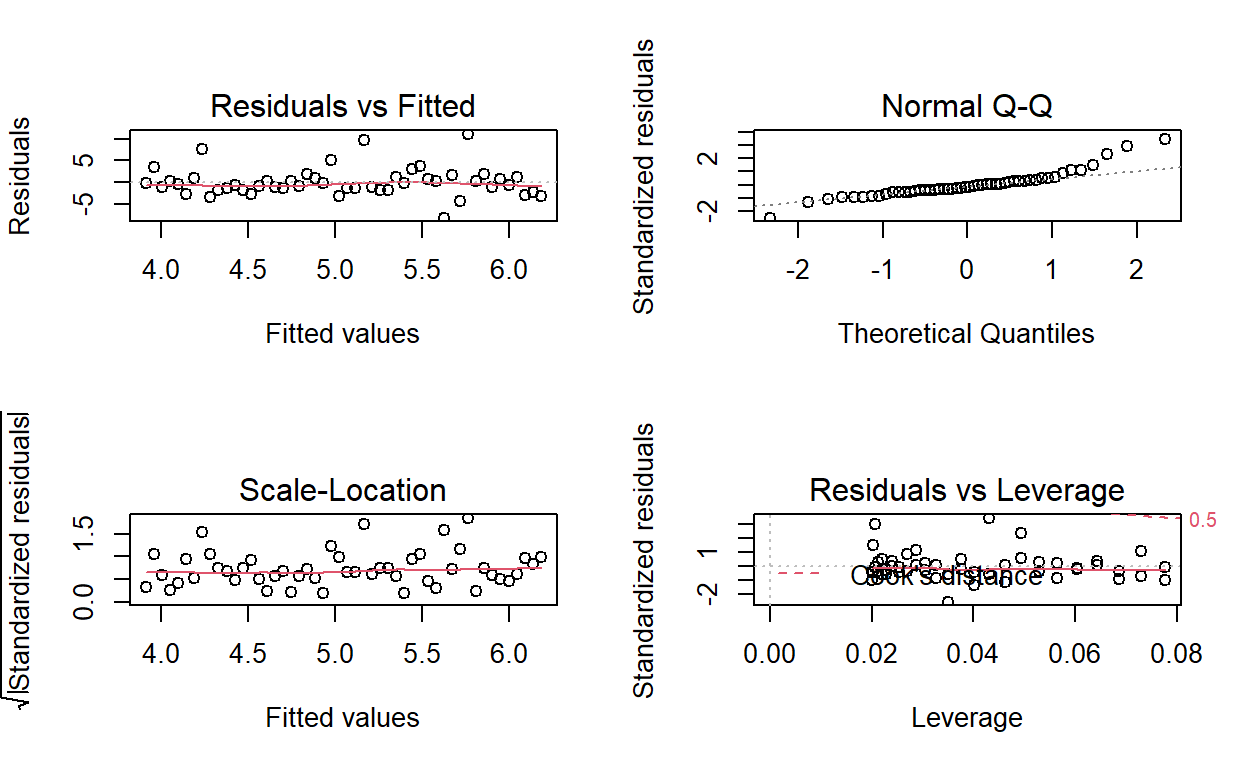

BT PQ P1.T2.20.20.3 Regression residual plost

standard lm() diagnostic plots: residual vs fitted, normal Q-Q, scale-location, residuals vs levereage

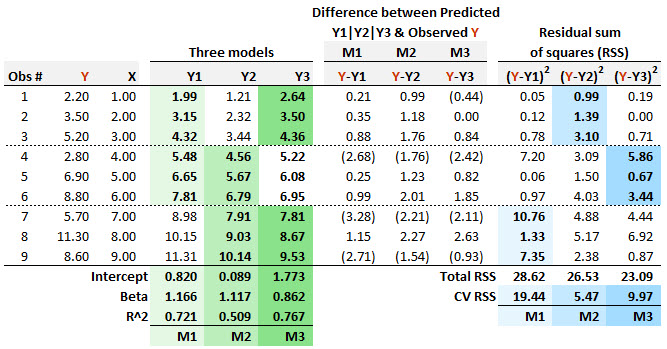

BT PQ P1.T2.20.20.2 Regression diagnostics: m-fold cross-validation (CV)

m-fold cross validation is for model checking, not model building

BT PQ P1.T2.20.20.1 Regression diagnostics: Cook's distance

Cook's distance evaluates an outlier

BT PQ P1-T2-20-19: Regression diagnostics (SET)

Diagnostics: omitted variable bias, heteroskedasticity, and multicollinearity

BT PQ P1-T2-20-18 (SET) Multivariate regressions

Fama-French three-factor model; House prices; and Medical costs

BT PQ P1-T2-20-17. Univariate regressions cont (2nd set v2)

Coefficient confidence interval (CI); hypothesis test; interpretation of SE, t-stat and p-value

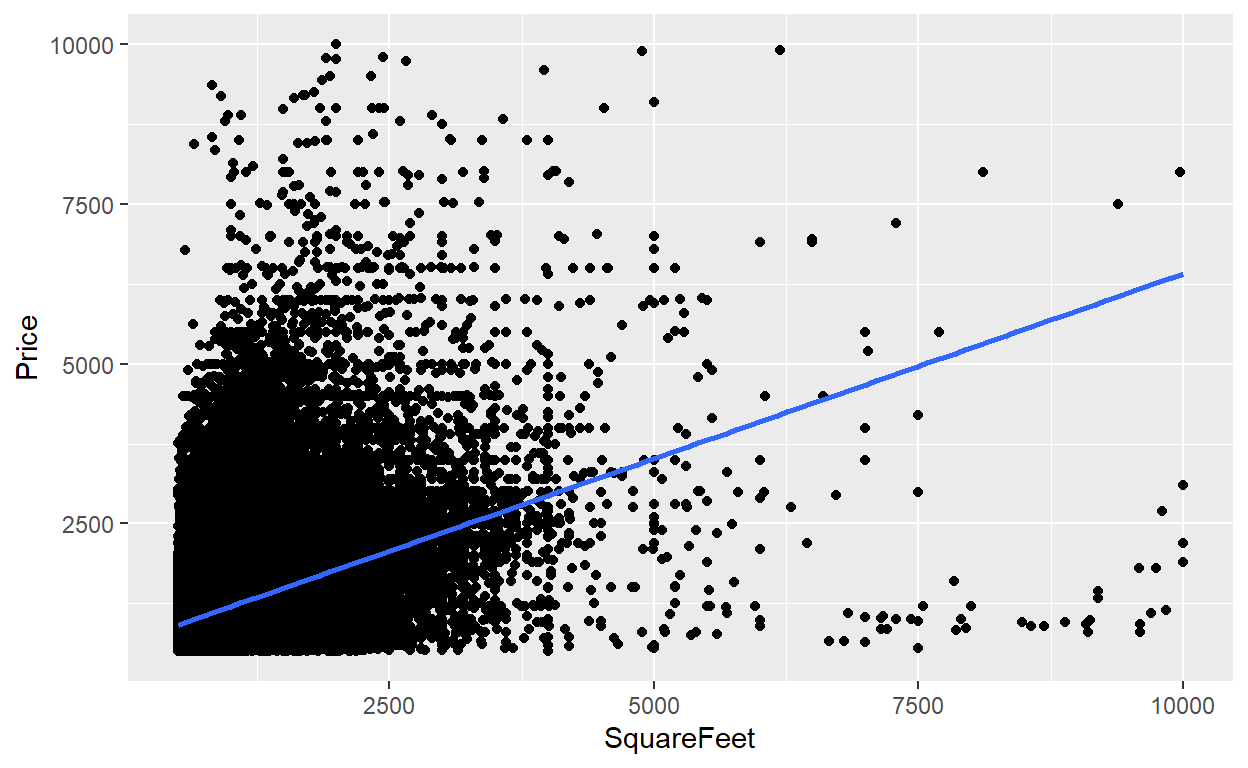

BT PQ P1-T2-20-16-3: Univariate regression: Monthly rental versus footage

Monthly rent against feet^2 per kaggle dataset

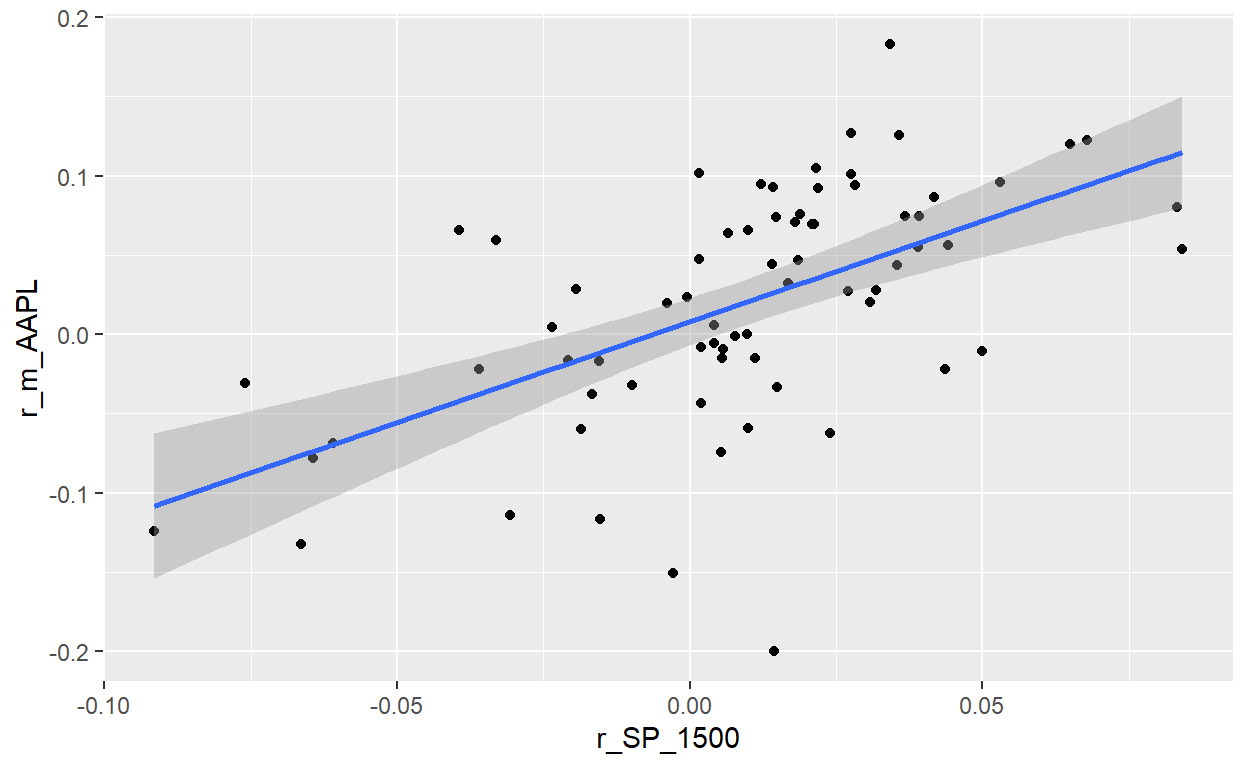

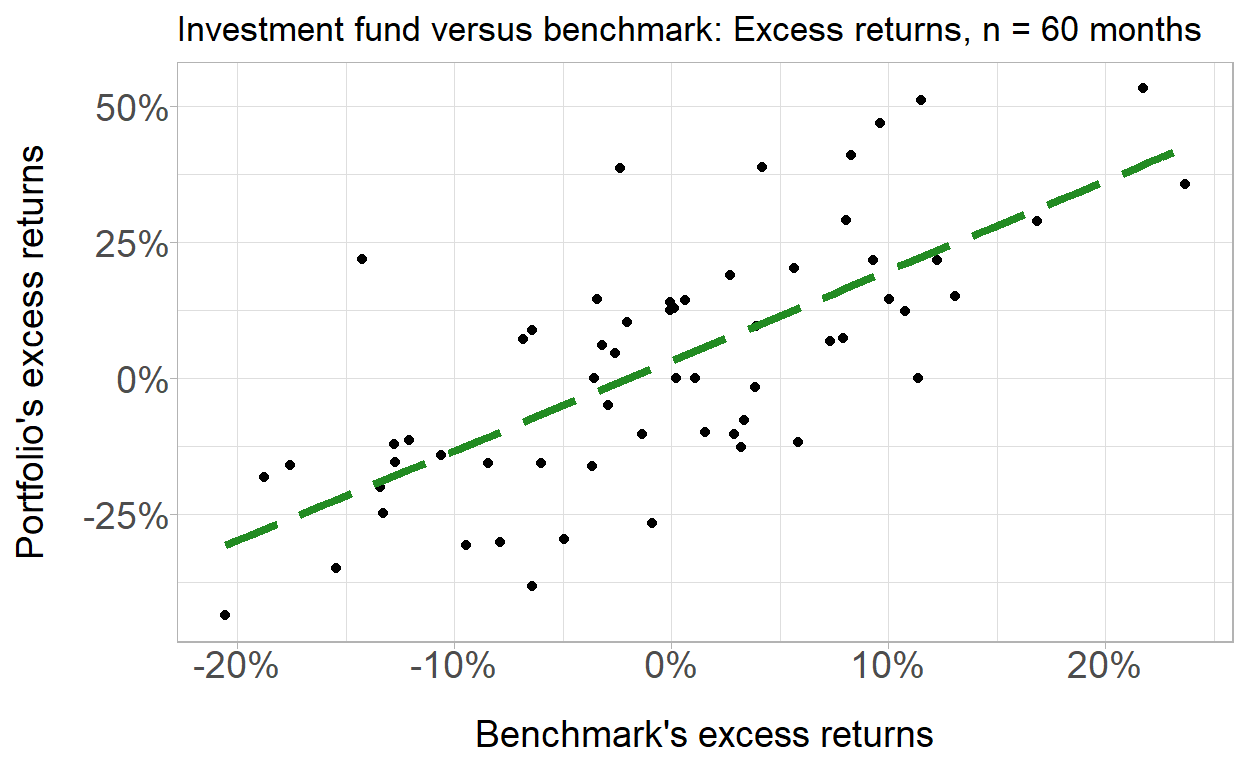

BT PQ P1-T2-20-16-2: Univariate regression: Portfolio versus benchmark returns

Simulated portfolio & benchmark for purposes of testing basic features of univariate regression

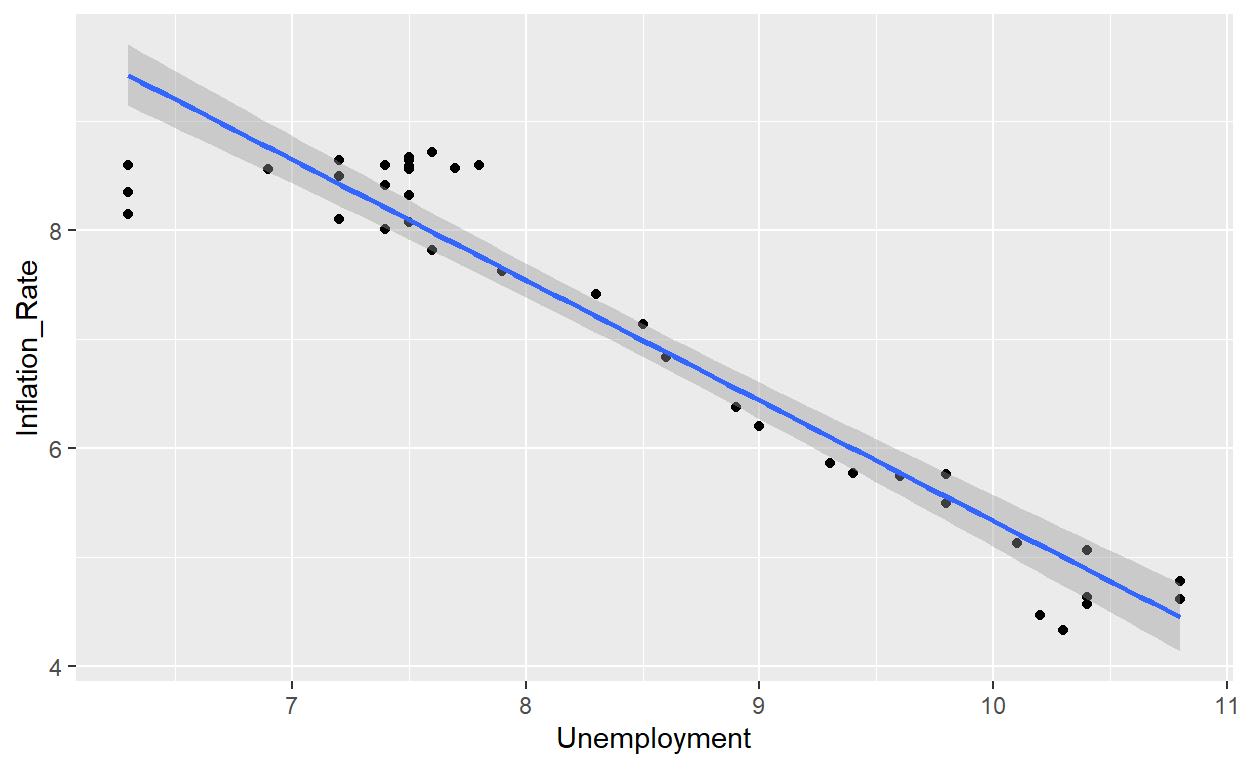

BT PQ P1-T2-20-16-1: Univariate regression: Inflation versus unemployment

With FRED data and applying gt_table

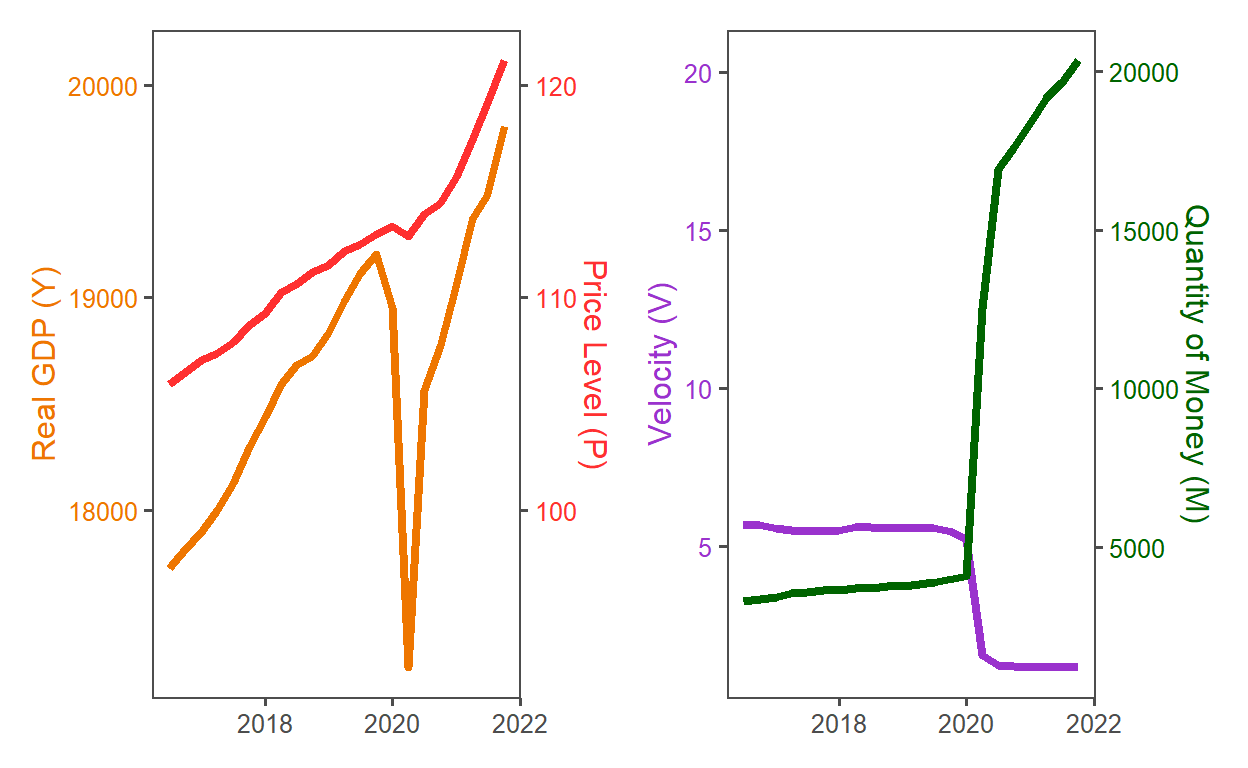

velocity of money

MV = PY illustrates the problem but is tautological

New distill site in 15 minutes

Distill is so much easier than blogdown