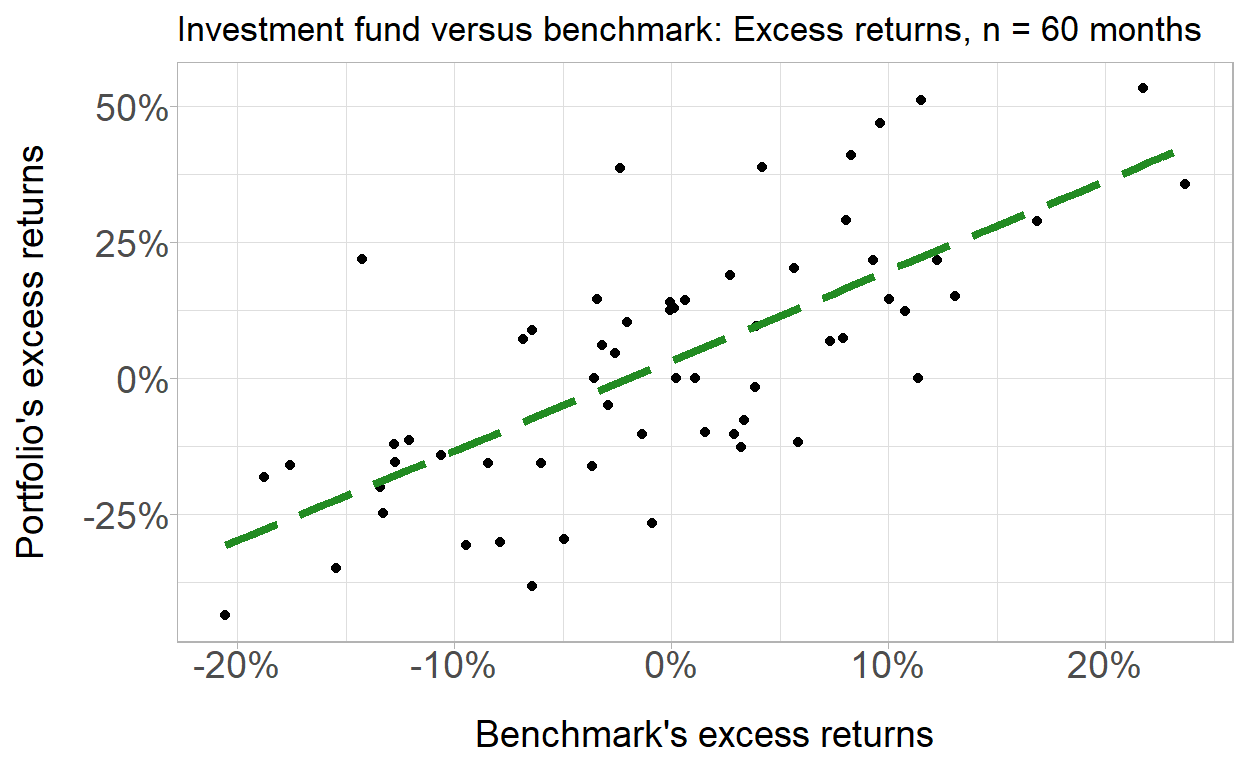

20.16.2. Peter is an analyst who is evaluating an investment fund whose managers claim has outperformed their benchmark. He collected monthly returns for the last five years; i.e., the sample size is excess return pairs over n = 60 months. He plots excess returns, which are defined as the returns in excess of the riskfree rate; ie., an excess return equals the gross return minus the riskfree rate. The scatterplot is displayed below:

scatterplot

The correlation coefficient is 0.708. In regard to the univariate data, the standard deviation of the portfolio’s returns is 22.84% and the standard deviation of the benchmark’s returns is 9.79%. The average excess return of the benchmark was -0.37% and the average excess return of the portfolio was 2.61%. Each of the following statements is true EXCEPT which is false?

- The slope of the regression line is approximately 1.65 and the intercept is approximately 3.22%

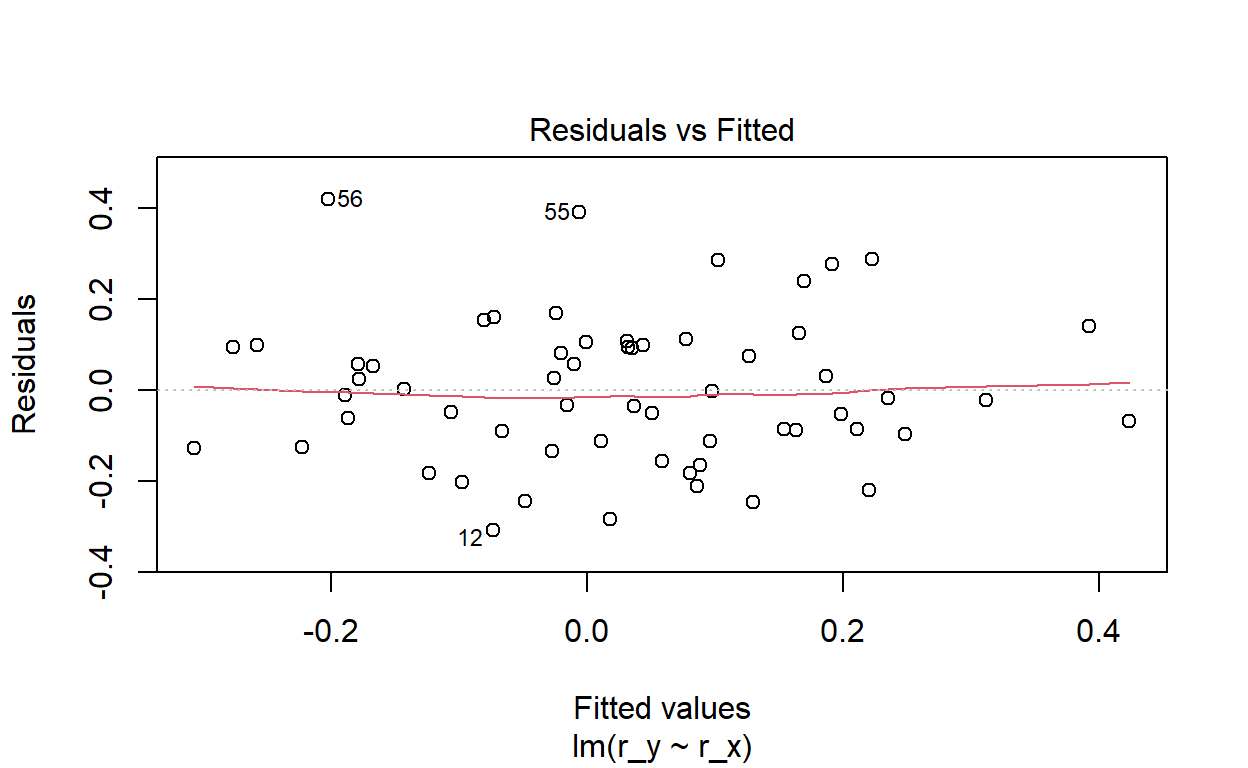

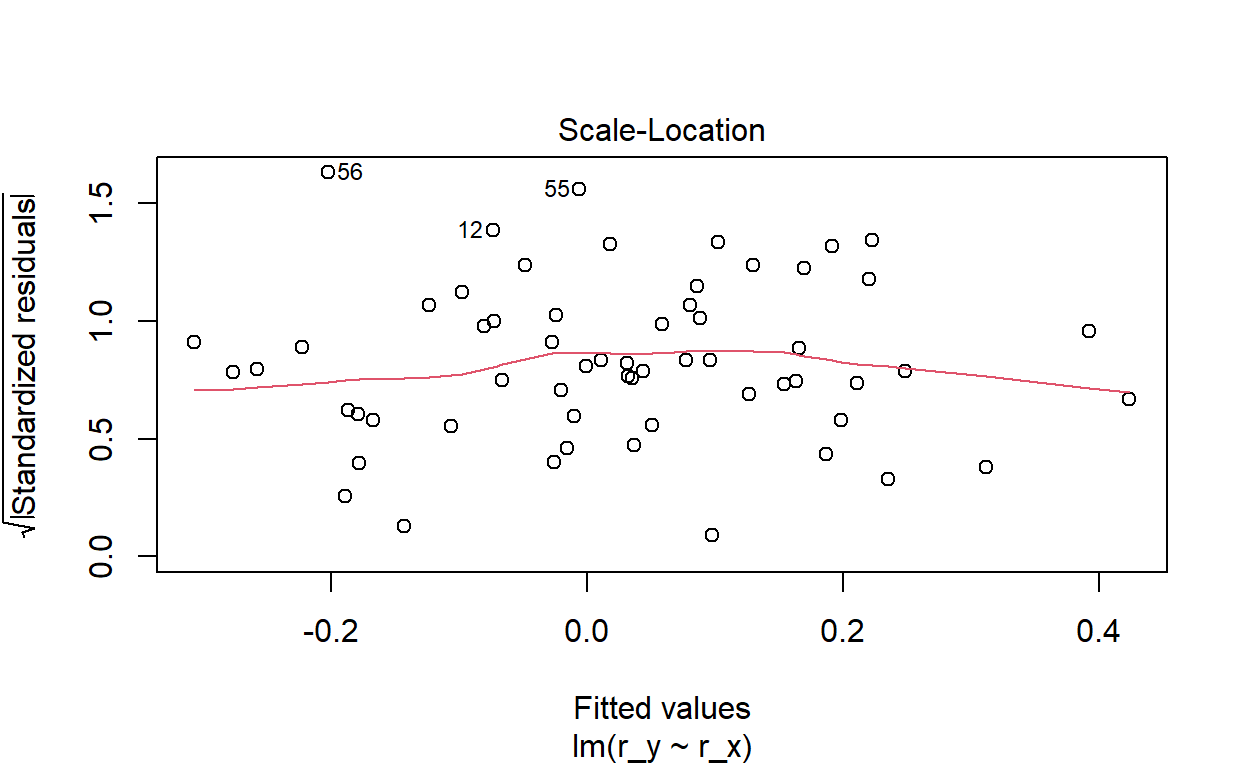

- Visual inspection confirms the error variance is not constant and we can, therefore, assert the presence of heteroskedastic shocks

- This regression line passes through the coordinates of averages, (μ_x, μ_y) = (-0.37%, +2.61%), although this is not an actual pairwise observation

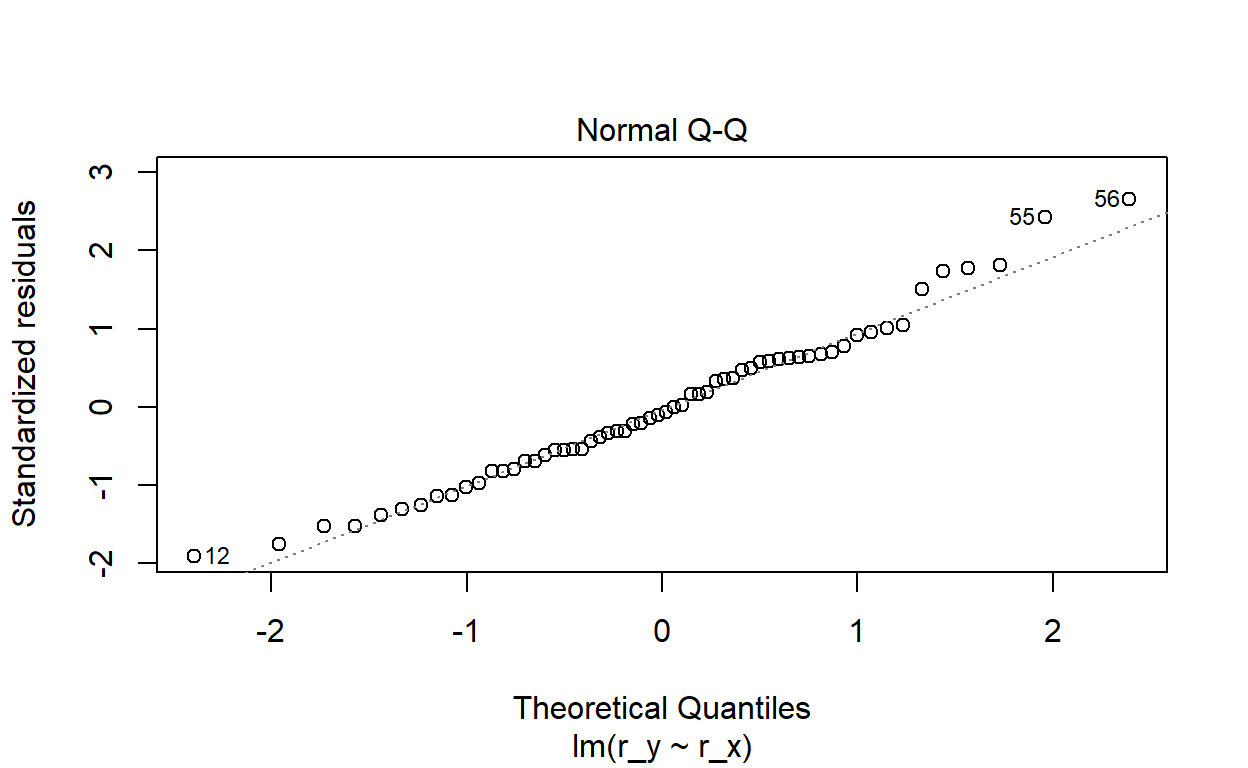

- This model appears to at least meet the three essential restrictions of a linear regression model including linearity in the coefficients (aka, parameters)

library(tidyverse)

library(scales)

library(ggthemes)

# library(lmtest)

x_mu <- .01; x_sig <- .1

y_mu <- .03; y_sig <- .2

rho <- 0.72

months <- 60

#set.seed(59)

set.seed(158)

# 60 rows of random standard normals

returns <- tibble(index = 1:months)

returns$x1 <- rnorm(months)

returns$y1 <- rnorm(months)

# make y2 correlated with y1; adjust location/scale

returns1 <- returns %>% mutate(

y2 = rho*x1 + sqrt(1 - rho^2)*y1,

r_x = x_mu + x1 * x_sig,

r_y = y_mu + y2 * y_sig

)

x_sd <- sd(returns1$r_x)

y_sd <- sd(returns1$r_y)

rho_xy <- cor(returns1$r_x, returns1$r_y)

beta_yx <- rho_xy * y_sd / x_sd

x_mu_act <- mean(returns1$r_x)

y_mu_act <- mean(returns1$r_y)

sprintf("sample rho is %.4f. The standard deviation of Portfolio returns is ", rho_xy)

[1] "sample rho is 0.7078. The standard deviation of Portfolio returns is "[1] "Portfolio standard deviation is 22.84%"[1] "Benchmark standard deviation is 9.79%"[1] "Portfolio average excess return is 2.61%"[1] "Benchmark average excess return is -0.37%"sprintf("Beta(P,B) is %.3f", beta_yx)

[1] "Beta(P,B) is 1.652"

Call:

lm(formula = r_y ~ r_x, data = returns1)

Residuals:

Min 1Q Median 3Q Max

-0.30810 -0.11231 -0.01385 0.09922 0.42134

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.03231 0.02102 1.537 0.13

r_x 1.65219 0.21649 7.632 2.54e-10 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.1627 on 58 degrees of freedom

Multiple R-squared: 0.501, Adjusted R-squared: 0.4924

F-statistic: 58.24 on 1 and 58 DF, p-value: 2.543e-10returns1 %>% ggplot(aes(x = r_x, y = r_y)) +

geom_point() +

geom_smooth(method = "lm", se = FALSE, color = "forestgreen", linetype = "longdash", size = 1.5) +

ggtitle("Investment fund versus benchmark: Excess returns, n = 60 months") +

xlab("Benchmark's excess returns") +

ylab("Portfolio's excess returns") +

scale_x_continuous(labels = percent_format(accuracy = 1)) +

scale_y_continuous(labels = percent_format(accuracy = 1)) +

theme_light() +

theme(

axis.title.y = element_text(size = 14),

axis.title.x = element_text(size = 14),

axis.text.x = element_text(size = 14, margin = margin(b = 10)),

axis.text.y = element_text(size = 14, margin = margin(l = 10))

)

plot(returns1_lm)

new.df <- data.frame(r_x = c(x_mu_act, 0, seq(from = 0.01, to = 0.1, by = .01)))

new.df$predicted_y <- predict(returns1_lm, new.df)

new.df

r_x predicted_y

1 -0.003740684 0.02613168

2 0.000000000 0.03231199

3 0.010000000 0.04883388

4 0.020000000 0.06535577

5 0.030000000 0.08187766

6 0.040000000 0.09839955

7 0.050000000 0.11492143

8 0.060000000 0.13144332

9 0.070000000 0.14796521

10 0.080000000 0.16448710

11 0.090000000 0.18100899

12 0.100000000 0.19753088intercept_predict <- (0 - x_mu_act)*beta_yx + y_mu_act

intercept_predict_round <- (0 - round(x_mu_act,4))*beta_yx + round(y_mu_act,4)

intercept_predict

[1] 0.03231199intercept_predict_round

[1] 0.0322131