Learning objectives

- Explain mean reversion and calculate a mean-reverting level.

- Define and describe the properties of autoregressive moving average (ARMA) processes.

- Describe the application of AR, MA and ARMA processes.

Let’s load some packages

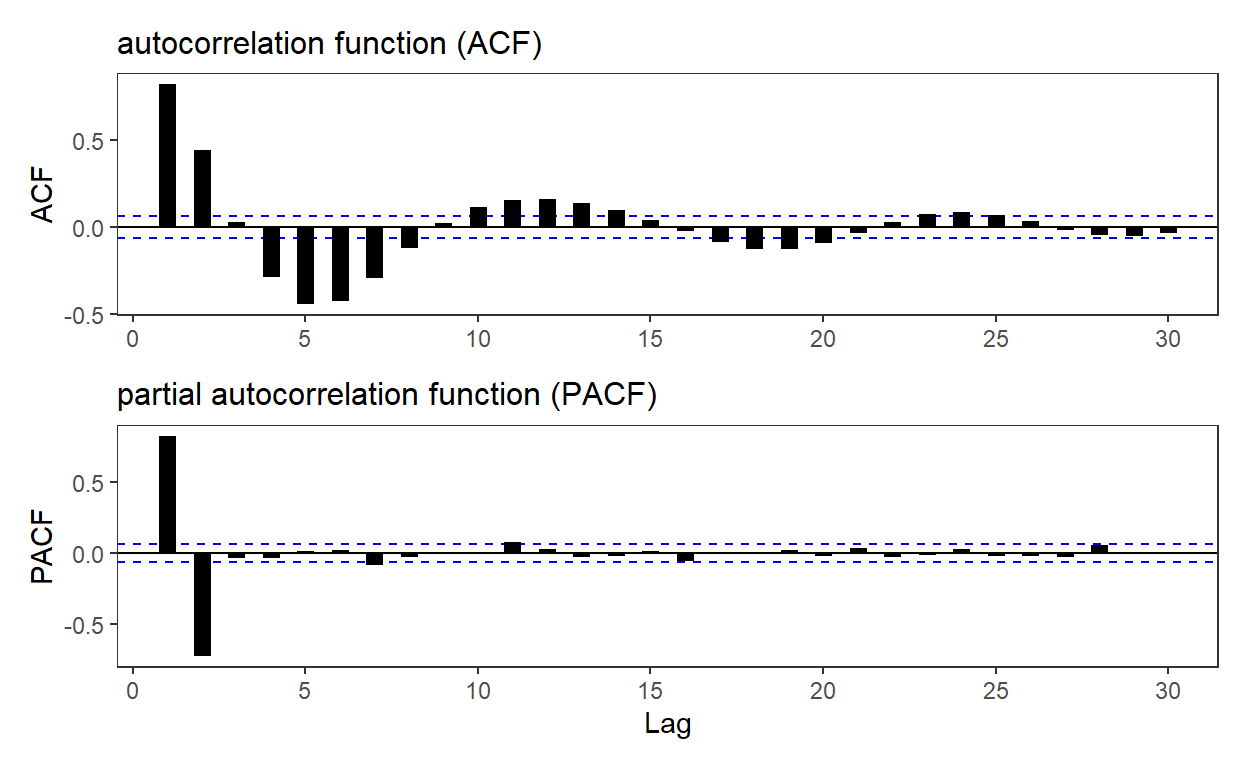

20.23.1. Below are plotted the autocorrelation function (ACF) and partial autocorrelation function (PACF) for a simulated time-series process. Please note that the horizontal dashed blue lines represent the 95.0% confidence interval … Which of the following time-series models is most likely described by these ACF and PACF plots?

set.seed(66)

AR_param_1 = 1.4

AR_param_2 = -0.7

AR_intercept = 0

AR_n <- 1000

theme_set(theme_bw())

# arima.sim model c(p, d, q)

# p = AR order

# d = difference

# q = MA order

# Generate an AR(2) with parameters, AR_param_1 and AR_param_2

AR <- arima.sim(model=list(order=c(2,0,0), ar = c(AR_param_1, AR_param_2)), n = AR_n, mean = AR_intercept)

p3 <- ggAcf(AR) +

geom_segment(size = 3) +

labs(

title = "autocorrelation function (ACF)"

) + theme(

plot.title = element_text(size = 12),

axis.title.x = element_blank(),

panel.grid = element_blank()

)

p4 <- ggPacf(AR) +

geom_segment(size = 3) +

labs(

title = "partial autocorrelation function (PACF)"

) + theme(

plot.title = element_text(size = 12),

panel.grid = element_blank()

)

# Please note plot is shrunk to 86% on copy/paste

p3 / p4

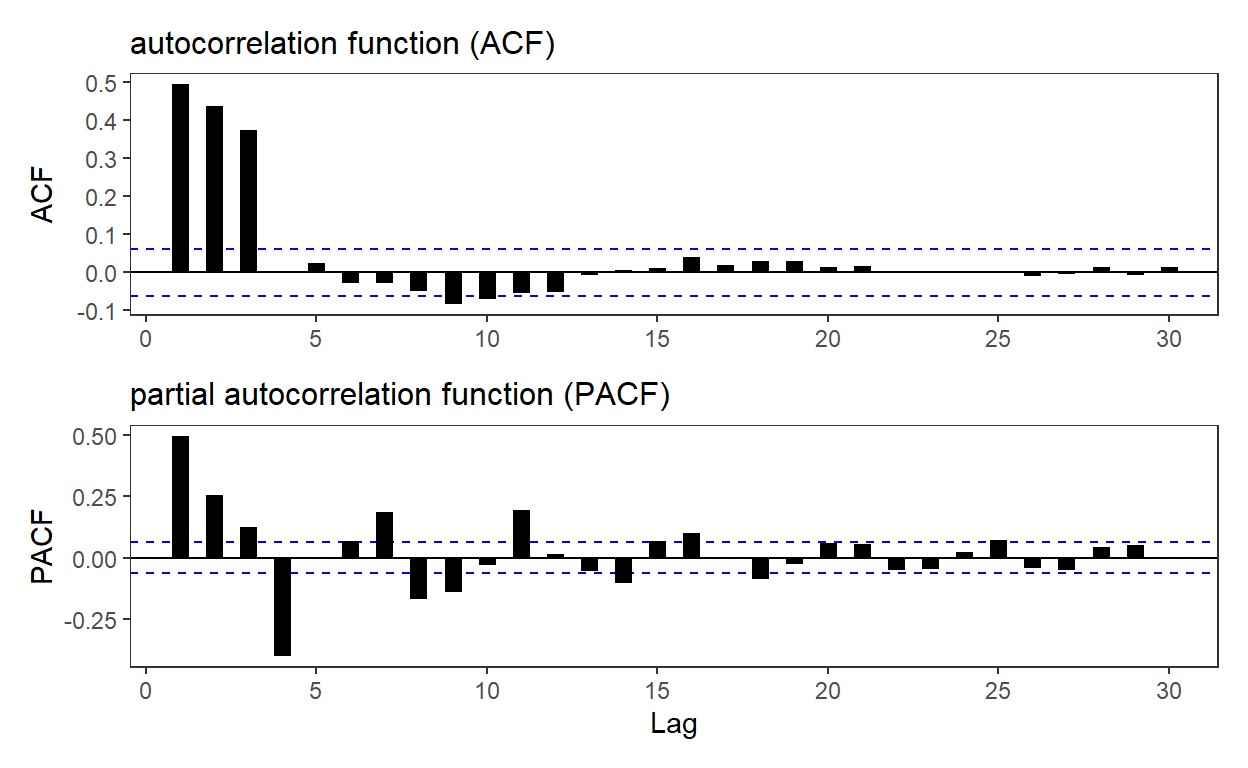

20.23.2. Below are plotted the autocorrelation function (ACF) and partial autocorrelation function (PACF) for a simulated time-series process. Please note that the horizontal dashed blue lines represent the 95.0% confidence interval … Which of the following time-series models is most likely described by these ACF and PACF plots?

set.seed(19)

MA_n = 1000

MA_mean = 0

MA_weight_1 = 0.4

MA_weight_2 = 0.6

MA_weight_3 = 0.8

# # Generate an MA(3) with weights MA_weight_1, MA_weight_2, and MA_weight_3

MA <- arima.sim(model=list(order = c(0,0,3), ma = c(MA_weight_1, MA_weight_2, MA_weight_3)), n = MA_n, mean = MA_mean)

p5 <- ggAcf(MA) +

geom_segment(size = 3) +

# geom_hline(yintercept = c(ci2, -ci2), color = "darkblue", linetype = "dashed", size = 2 ) +

labs(

title = "autocorrelation function (ACF)"

) + theme(

plot.title = element_text(size = 12),

axis.title.x = element_blank(),

panel.grid = element_blank()

)

p6 <- ggPacf(MA) +

geom_segment(size = 3) +

labs(

title = "partial autocorrelation function (PACF)"

) + theme(

plot.title = element_text(size = 12),

panel.grid = element_blank()

)

# Please note plot is shrunk to 86% on copy/paste

p5 / p6

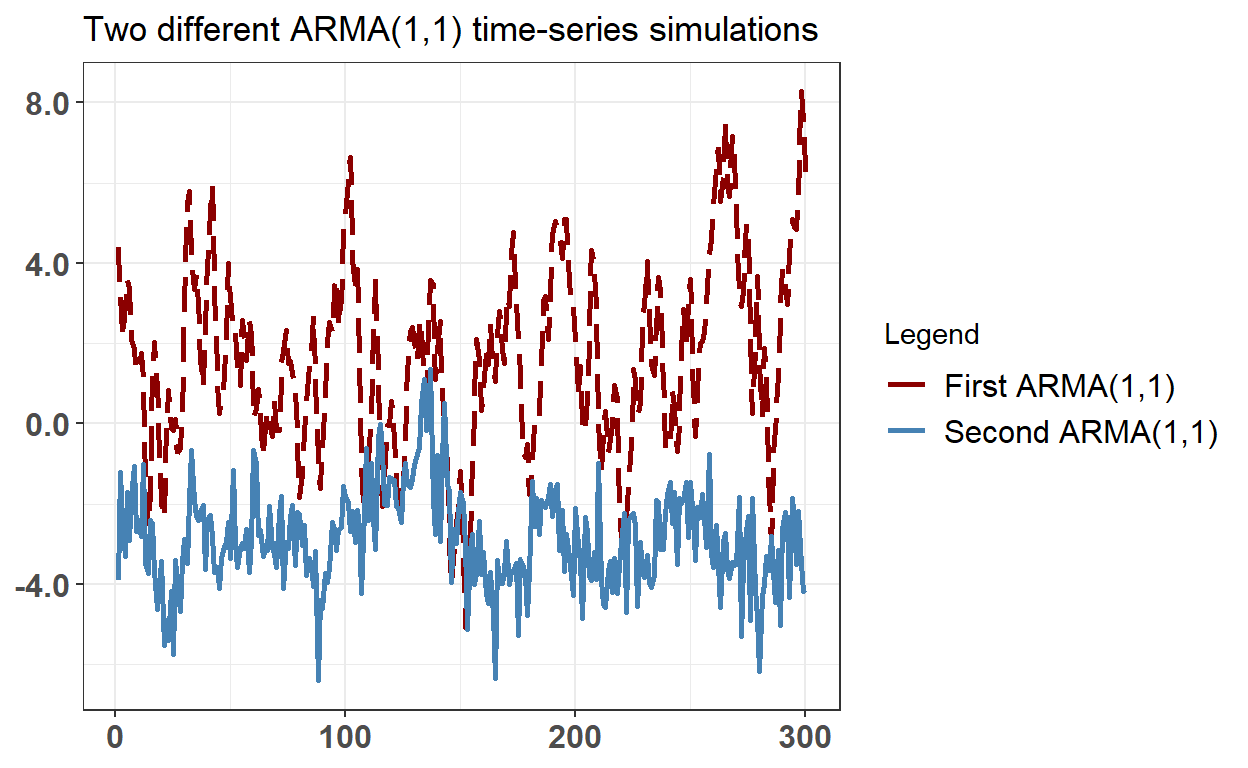

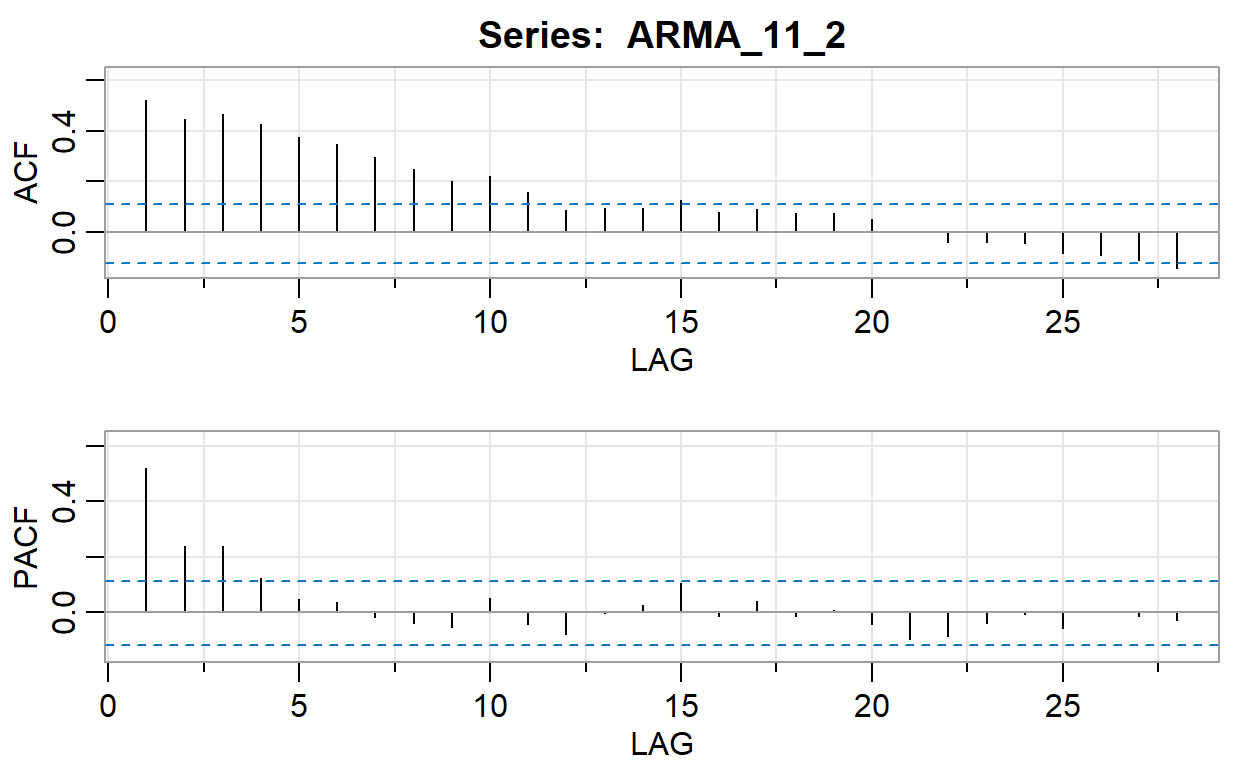

20.23.3. An ARMA(1,1) process evolves according to Y(t) = ẟ + ϕ*Y(t-1) + θ*ε(t-1) + ε(t). The plot below contains two 300-step ARMA(1,1) processes that differ only in their coefficients …

Which of the following statements is TRUE about the two ARMA(1,1) simulations above?

- Both of the ARMA(1,1) processes are likely to exhibit slow decay in both the ACF and PACF

- Both of the ARMA(1,1) processes are likely to cut off sharply at lag 1 in both the ACF and PACF

- The first ARMA(1,1) process (i.e., plotted with a red dashed line) cannot be covariance-stationary

- The unconditional mean of both ARMA(1,1) processes must be zero because all ARMA(1,1) have a long-run mean of zero

library(astsa)

set.seed(9)

ar_11_1 = 0.8

ma_11_1 = 0.6

arma_11_1_mu = 2

sim_n = 300

ar_11_2 = 0.9

ma_11_2 = -0.5

arma_11_2_mu = -3

# ar_22 = c(1.4, -0.6)

# ma_22 = c(0.9, 0.6)

ARMA_11_1 <- arima.sim(model=list(order = c(1, 0, 1), ar = ar_11_1, ma = ma_11_1), n = sim_n) + arma_11_1_mu

ARMA_11_2 <- arima.sim(model=list(order = c(1, 0, 1), ar = ar_11_2, ma = ma_11_2), n = sim_n) + arma_11_2_mu

# ARMA_22 <- arima.sim(model=list(order = c(2, 0, 2), ar = ar_22, ma = ma_22), n = 200)

# ts.plot(ARMA_11, ARMA_22)

time_arma <- bind_cols(ARMA_11_1, ARMA_11_2) %>% rowid_to_column() %>%

rename(y_ARMA_11_1 = ...1, y_ARMA_11_2 = ...2)

theme_set(theme_bw())

colors <- c("First ARMA(1,1)" = "darkred", "Second ARMA(1,1)" = "steelblue")

time_arma %>% ggplot(aes(x = rowid)) +

geom_line(aes(y = y_ARMA_11_1, color = "First ARMA(1,1)"), size = 1, linetype = "longdash") +

geom_line(aes(y = y_ARMA_11_2, color = "Second ARMA(1,1)"), size = 1) +

scale_y_continuous(labels = scales::number_format(accuracy = 0.1)) +

theme(

axis.title.y = element_blank(),

axis.title.x = element_blank(),

axis.text.x = element_text(size = 12, face = "bold"),

axis.text.y = element_text(size = 12, face = "bold"),

legend.position = "right",

legend.text = element_text(size = 12)

) + labs(

title = "Two different ARMA(1,1) time-series simulations",

color = "Legend"

) +

scale_color_manual(values = colors)

arma_11_1_mulr = arma_11_1_mu/(1 - ar_11_1)

arma_11_2_mulr = arma_11_2_mu/(1 - ar_11_2)

# mu_arma_22 = 10

#ARMA_22 <- arima.sim(model=list(order = c(2, 0, 2), ar = c(0.4, 0.2), ma = c(0.5,0.6)), n = 200, mean = mu_arma_22)

# ts.plot(ARMA_22)

# acf2(ARMA_22)

# mean_arma_22 = mu_arma_22/(1 - 0.4 - 0.2)

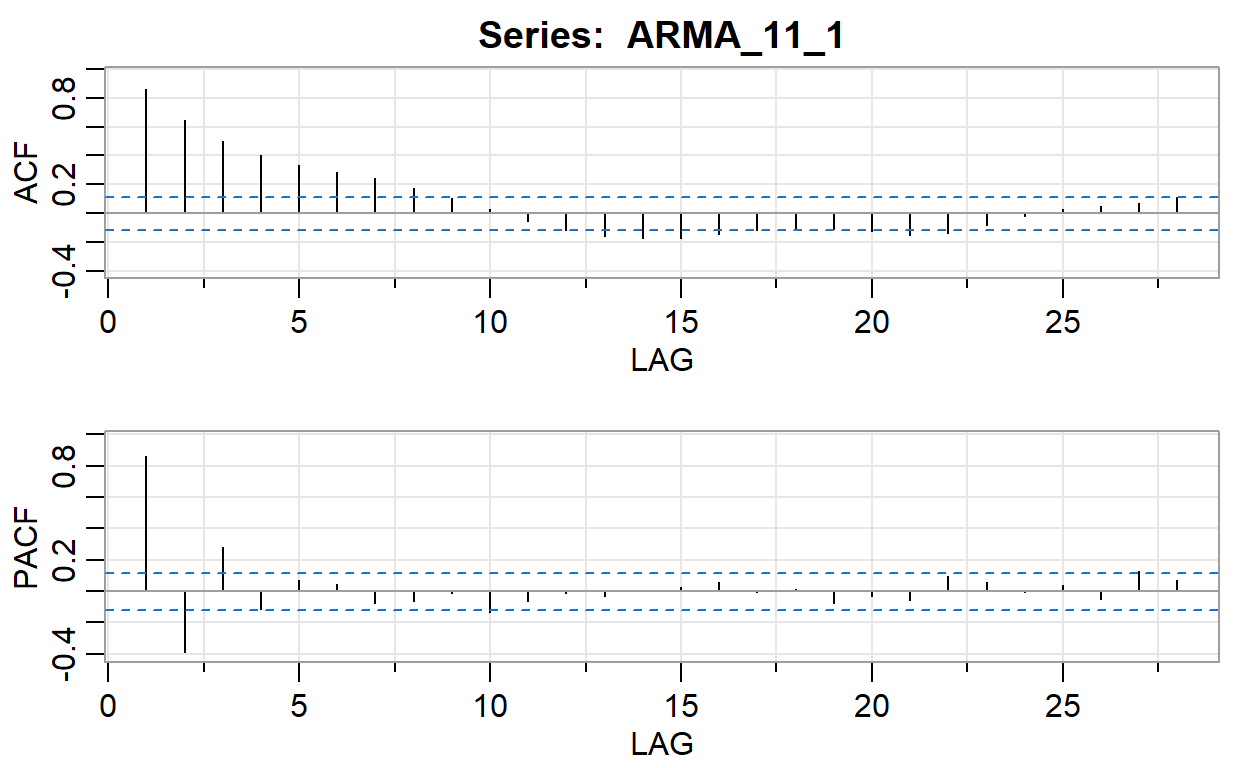

acf2(ARMA_11_1)

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11]

ACF 0.86 0.65 0.50 0.40 0.33 0.29 0.24 0.18 0.11 0.03 -0.05

PACF 0.86 -0.39 0.28 -0.11 0.07 0.05 -0.07 -0.06 -0.01 -0.13 -0.06

[,12] [,13] [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21]

ACF -0.12 -0.16 -0.17 -0.17 -0.15 -0.12 -0.10 -0.11 -0.13 -0.15

PACF -0.01 -0.03 0.01 0.03 0.06 0.00 0.01 -0.08 -0.03 -0.05

[,22] [,23] [,24] [,25] [,26] [,27] [,28]

ACF -0.14 -0.08 -0.02 0.03 0.05 0.07 0.11

PACF 0.10 0.06 0.00 0.04 -0.05 0.13 0.07acf2(ARMA_11_2)

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11]

ACF 0.52 0.45 0.46 0.43 0.37 0.35 0.30 0.25 0.20 0.22 0.16

PACF 0.52 0.24 0.24 0.12 0.05 0.04 -0.02 -0.04 -0.05 0.05 -0.04

[,12] [,13] [,14] [,15] [,16] [,17] [,18] [,19] [,20] [,21]

ACF 0.09 0.09 0.10 0.13 0.08 0.09 0.08 0.07 0.05 0.00

PACF -0.08 0.00 0.03 0.10 -0.01 0.04 -0.01 0.01 -0.04 -0.09

[,22] [,23] [,24] [,25] [,26] [,27] [,28]

ACF -0.04 -0.04 -0.04 -0.08 -0.09 -0.11 -0.14

PACF -0.09 -0.04 -0.01 -0.06 0.00 -0.01 -0.03end of post