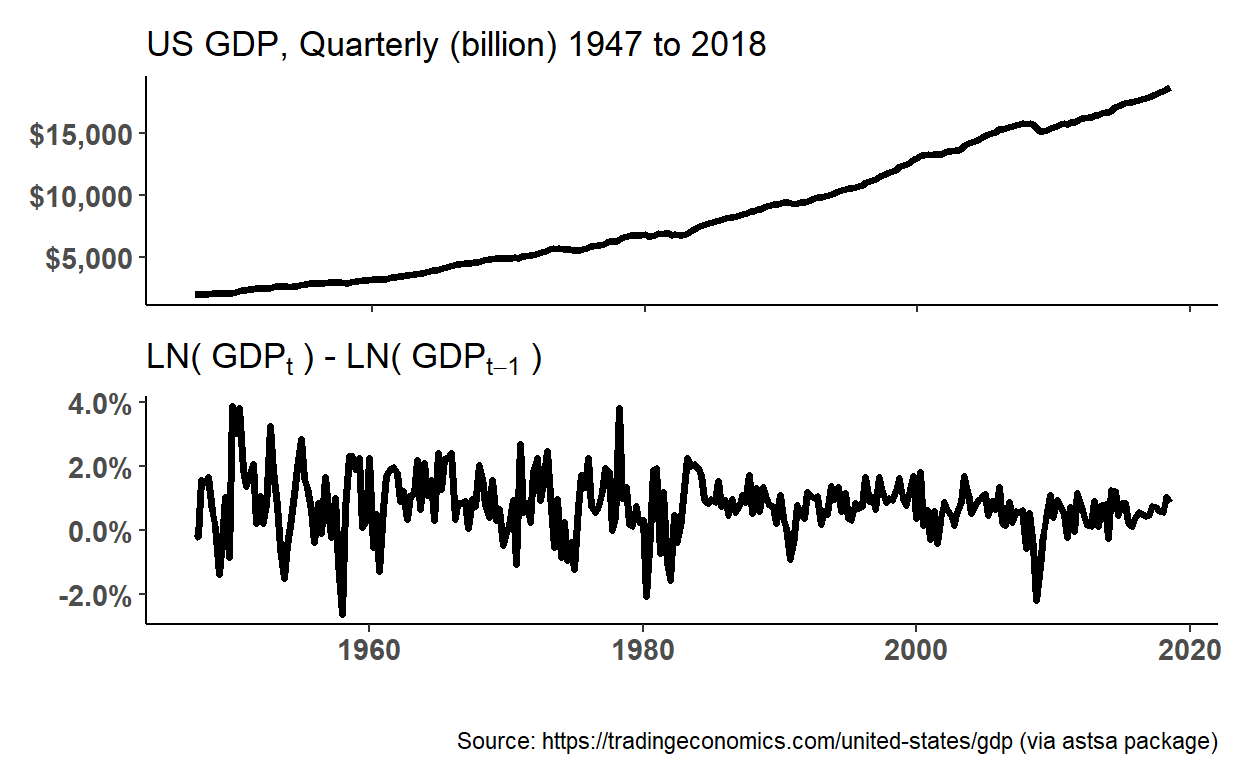

20.24.2. Elizabeth is an economist tasked with modeling quarterly gross domestic product (GDP) in the United States. She starts with the plots displayed below. The raw data is displayed in the upper; she observes this GDP trend is obviously not stationary (why?). She then performs a typical transformation on the raw data: she takes the difference of the natural log of the quarterly GPD values. This plot is displayed in the lower panel. Because LN[GDP(t)] - LN(GDP(t-1)] = LN[GDP(t)/GDP(t-1)], this lower panel plots continuously compounded returns (aka, monthly log returns). First differencing the log returns occasionally renders the non-stationary trend into a stationary process.

library(tidyverse)

library(scales)

library(forecast)

library(tseries)

library(ggthemes)

library(ggfortify)

library(fpp2)

library(gt)

library(astsa)

library(patchwork)

# library(gridExtra)

gdp_log <- diff(log(gdp))

# ts.plot(gdp)

# ts.plot(gdp_log)

p1_gdp <- autoplot(gdp, size = 1.3) + labs(

title = "US GDP, Quarterly (billion) 1947 to 2018"

) + theme_classic() + theme(

axis.title.x = element_blank(),

axis.title.y = element_blank(),

axis.text.x = element_blank(),

axis.text.y = element_text(size = 11, face = "bold")

) + scale_y_continuous(labels = dollar_format())

p2_gdp_log <- autoplot(gdp_log, size = 1.3) + labs(

title = bquote("LN("~GDP[t]~ ") - LN("~GDP[t-1]~")")

) + theme_classic() + theme(

axis.title.y = element_blank(),

axis.text.x = element_text(size = 11, face = "bold"),

axis.text.y = element_text(size = 11, face = "bold")

) + scale_y_continuous(labels = label_percent(accuracy = .1))

patchwork <- p1_gdp / p2_gdp_log

patchwork + plot_annotation(

caption = "Source: https://tradingeconomics.com/united-states/gdp (via astsa package)"

)

(on to the Box-Pierce…)

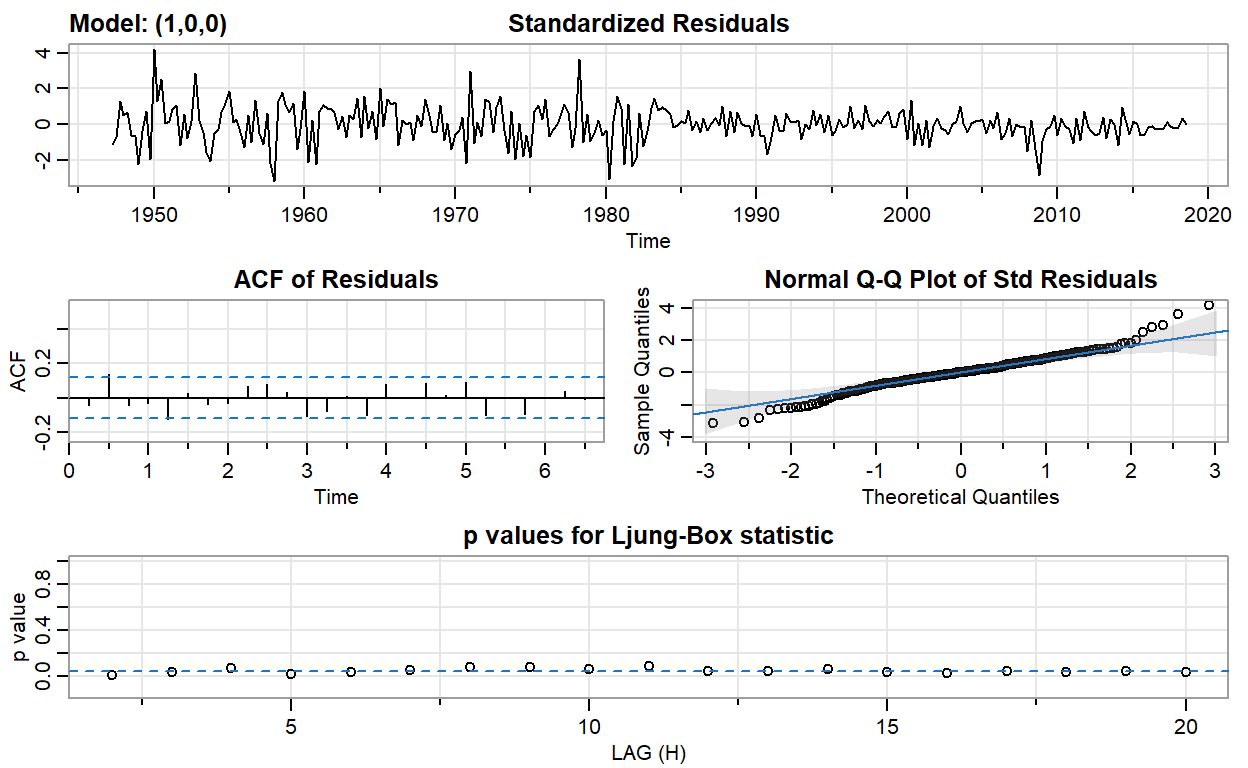

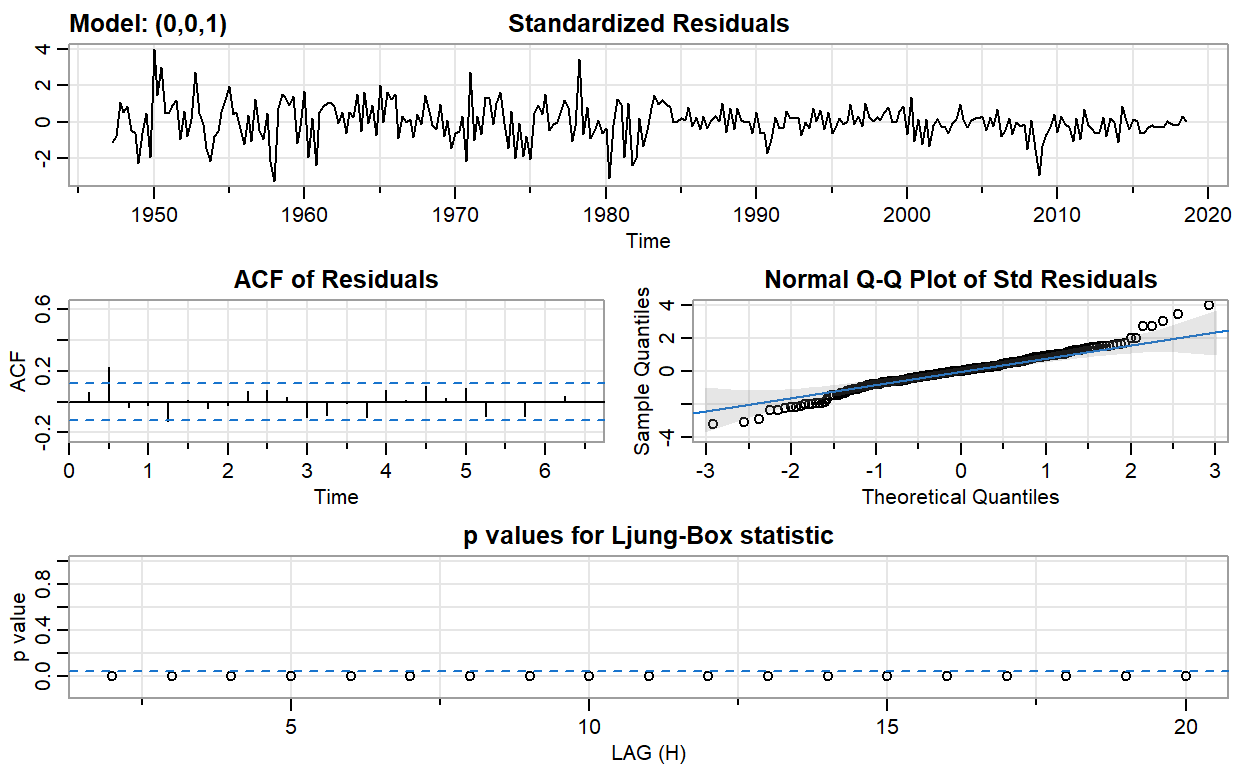

She then fits an autoregressive, AR(1), and moving average, MA(1), model to the log return series. This gives her three models: the log return series (called “diff_logs”), an AR(1) model, and an MA(1) model. She conducts a Box-Pierce test on each of these models; the test of the AR(1) and MA(1) is a test of the residuals. She selects two lags for the test, h = 10 and h = 20. The results of her Box-Pierce test are displayed below.

… Box-Pierce gt table (below) here …

If we assume her desired confidence level is 95.0%, which of the following statements is a TRUE statement with respect to an interpretation of her Box-Pierce test of the three models?

- None of the residuals are white noise; i.e., neither the transformed log returns nor AR(1) nor MA(1) is a candidate model

- The AR(1) is a candidate because its residuals appear to be approximately white noise

- The MA(a) is a candidate because its residuals appear to be approximately white noise

- All of the residuals are white noise; i.e., all three models are candidates

# install.packages("kableExtra")

# install.packages("gapminder")

ar1_gdp_log <- sarima(gdp_log, p = 1, d = 0, q = 0)

initial value -4.673186

iter 2 value -4.742918

iter 3 value -4.742921

iter 4 value -4.742923

iter 5 value -4.742925

iter 6 value -4.742925

iter 6 value -4.742925

final value -4.742925

converged

initial value -4.742229

iter 2 value -4.742234

iter 3 value -4.742245

iter 3 value -4.742245

iter 3 value -4.742245

final value -4.742245

converged

ma1_gdp_log <- sarima(gdp_log, p = 0, d = 0, q = 1)

initial value -4.672758

iter 2 value -4.716609

iter 3 value -4.723220

iter 4 value -4.723481

iter 5 value -4.723483

iter 5 value -4.723483

iter 5 value -4.723483

final value -4.723483

converged

initial value -4.723444

iter 1 value -4.723444

final value -4.723444

converged

ma2_gdp_log <- sarima(gdp_log, p = 0, d = 0, q = 2)

initial value -4.672758

iter 2 value -4.749239

iter 3 value -4.750696

iter 4 value -4.750723

iter 5 value -4.750724

iter 6 value -4.750725

iter 7 value -4.750725

iter 7 value -4.750725

iter 7 value -4.750725

final value -4.750725

converged

initial value -4.751078

iter 2 value -4.751080

iter 3 value -4.751080

iter 4 value -4.751081

iter 5 value -4.751081

iter 5 value -4.751081

iter 5 value -4.751081

final value -4.751081

converged

h_values <- c(10, 20)

# diff of logs

model = "diff_logs"

results_log_list <- h_values %>% map(~Box.test(gdp_log, lag = .))

log_statistic <- results_log_list %>% map_dbl("statistic")

log_p.value <- results_log_list %>% map_dbl("p.value")

log_cols <- data.frame(cbind(h_values, log_statistic, log_p.value))

log_all <- cbind(model, log_cols)

log_all <- log_all %>% rename(

'h (lags)' = h_values,

statistic = log_statistic,

'p-value' = log_p.value

)

# AR(1)

model = "AR(1)"

results_ar1_list <- h_values %>% map(~Box.test(ar1_gdp_log$fit$residuals, lag = .))

ar1_statistic <- results_ar1_list %>% map_dbl("statistic")

ar1_p.value <- results_ar1_list %>% map_dbl("p.value")

ar1_cols <- data.frame(cbind(h_values, ar1_statistic, ar1_p.value))

ar1_all <- cbind(model, ar1_cols)

ar1_all <- ar1_all %>% rename(

'h (lags)' = h_values,

statistic = ar1_statistic,

'p-value' = ar1_p.value

)

# MA(1)

model = "MA(1)"

results_ma1_list <- h_values %>% map(~Box.test(ma1_gdp_log$fit$residuals, lag = .))

ma1_statistic <- results_ma1_list %>% map_dbl("statistic")

ma1_p.value <- results_ma1_list %>% map_dbl("p.value")

ma1_cols <- data.frame(cbind(h_values, ma1_statistic, ma1_p.value))

ma1_all <- cbind(model, ma1_cols)

ma1_all <- ma1_all %>% rename(

'h (lags)' = h_values,

statistic = ma1_statistic,

'p-value' = ma1_p.value

)

models_all <- rbind(log_all, ar1_all, ma1_all)

models_gt <- gt(models_all)

models_gt <-

models_gt %>%

tab_options(

table.font.size = 14

) %>% tab_style(

style = cell_text(weight = "bold"),

locations = cells_body()

) %>% tab_style(

style = cell_text(color = "cadetblue"),

locations = cells_column_labels(

columns = vars(model, 'h (lags)', statistic, 'p-value')

)

) %>% tab_header(

title = md("**Box-Pierce test statistics and p-values**"),

subtitle = "AR(1) and MA(1) at lags of h = 10 and 20"

) %>% fmt_number(

columns = vars(statistic, 'p-value'),

decimals = 4

) %>% tab_source_note(

source_note = md("Note: diff_logs = LN[GDP(t)] - LN[GPD(t-1)]")

) %>% tab_source_note(

source_note = md("AR(1) and MA(1) are tests of residuals")

) %>% cols_width(

vars(model, 'h (lags)') ~ px(80),

vars(statistic, 'p-value') ~ px(90)

) %>% cols_label (

model = md("**model**"),

'h (lags)' = md("**h (lags)**"),

statistic = md("**test stat**"),

'p-value' = md("**p-value**")

) %>% cols_align(

align = "center",

columns = vars('h (lags)')

) %>% tab_options(

heading.title.font.size = 16,

heading.subtitle.font.size = 14

)

models_gt

| Box-Pierce test statistics and p-values | |||

|---|---|---|---|

| AR(1) and MA(1) at lags of h = 10 and 20 | |||

| model | h (lags) | test stat | p-value |

| diff_logs | 10 | 62.6228 | 0.0000 |

| diff_logs | 20 | 80.1439 | 0.0000 |

| AR(1) | 10 | 15.5465 | 0.1134 |

| AR(1) | 20 | 30.3091 | 0.0650 |

| MA(1) | 10 | 24.3689 | 0.0067 |

| MA(1) | 20 | 39.6618 | 0.0055 |

| Note: diff_logs = LN[GDP(t)] - LN[GPD(t-1)] | |||

| AR(1) and MA(1) are tests of residuals | |||